In today’s issue:

- The surprising stats behind gold’s meteoric rise

- What should we compare gold to: bonds, stocks or crypto?

- Top global experts share their view with us

We’re almost a quarter of the way into the 21st century.

This has allowed some commentators to zoom out and look at the 25-year view of markets since 2000. That was an auspicious time, just before the internet bubble peaked, burst and collapsed in the US.

All this provides us with good lessons on the greatest trick in finance: chart crime.

Dates matter. For example, the US stock market’s 20-year average annual return (based on the S&P 500) is 8.7%. However, its 25-year return (from 1 January 2000) is a somewhat disappointing 5.8%. Over just the last decade though, it is a much happier 11.3%. Which is the best “average return” for stocks?

It matters, because when you compare something like gold to stocks, you can argue that either one outperformed the other (and therefore is “better”) depending on which dates you choose.

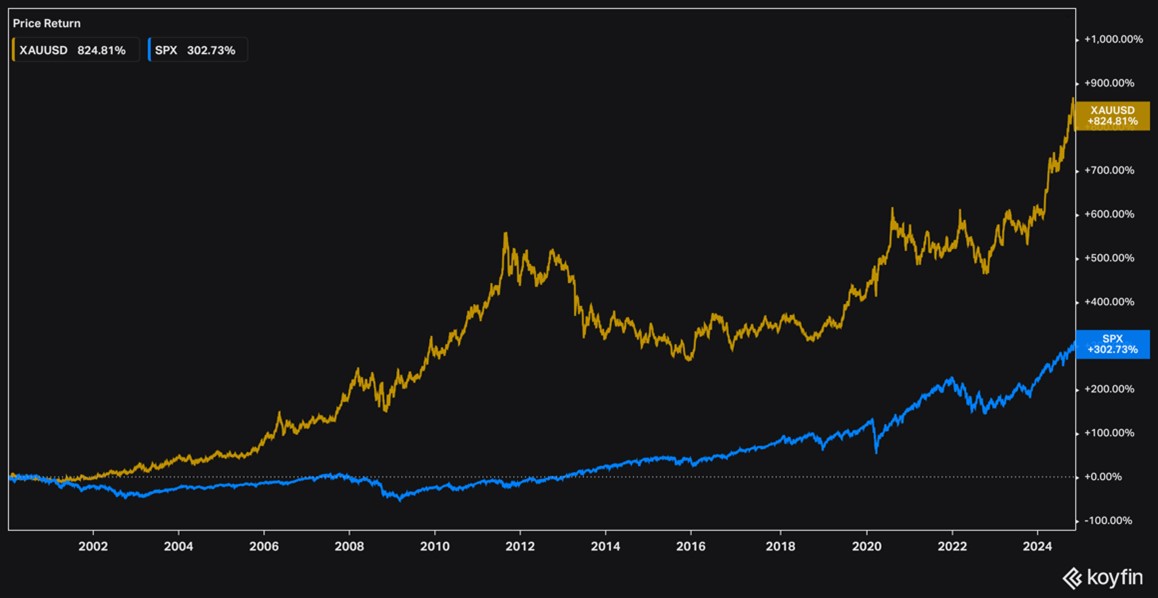

And so you can see that gold has returned almost triple the US stock market (blue) since 1 January 2000:

Source: Koyfin

Source: Koyfin

Compared to the S&P’s 5.8% return, gold has averaged 9.3% annually. Through compounding, that adds up to a huge different a quarter century later.

You might think that starting from the top of a stock market bubble is chart crime… but gold has also beaten it over 20 years, from nearer the market bottom after the tech bust:

Source: Koyfin

Source: Koyfin

In fact, the last decade is unusual as a period in which US stocks beat gold’s returns. 1980 to 2000 was the other glorious period for stocks, measured in gold.

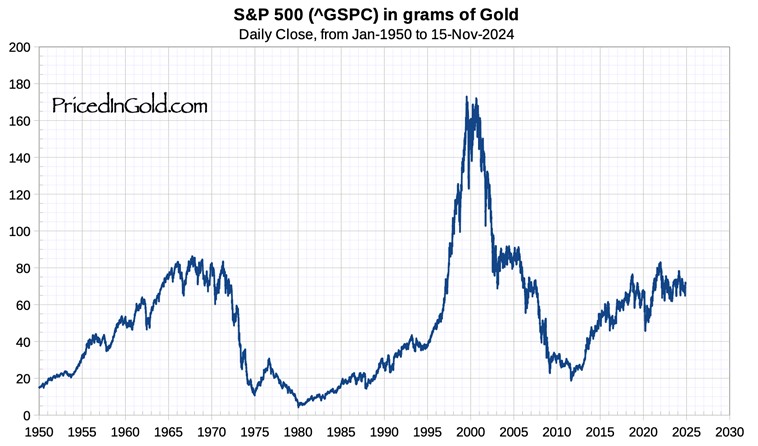

In fact, quite remarkably, if you price the S&P 500 in gold terms rather than dollars, it has gone absolutely nowhere in 60 years, albeit with some wild swings along the way:

Source: Priced In Gold

Source: Priced In Gold

This shows us that stocks haven’t necessarily done as well as people think. The dollar has just lost so much purchasing power, while gold has retained it. In gold terms, the S&P has been in a bear market since 1999.

But it doesn’t have to be one vs the other. They can work together. Gold’s traditional role has been as a hedge, or as a diversifier. The theory is that people seek its safety during times of crisis in the stock market.

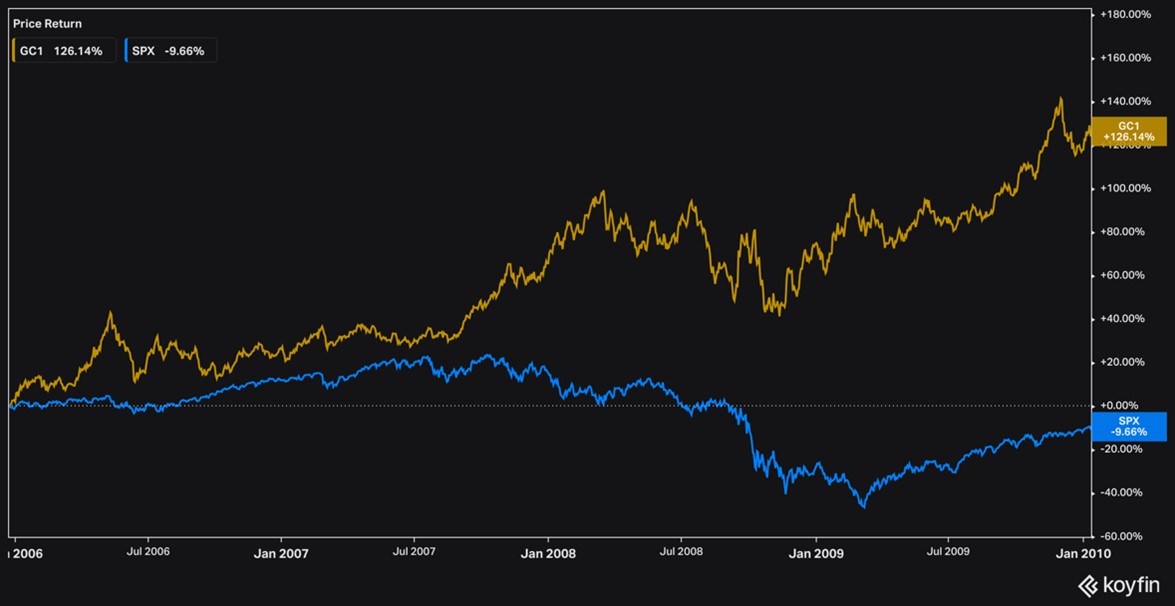

It performed this role admirably in between 2006 and 2010, showing resilience and even strength as the S&P 500 fell:

Source: Koyfin

Source: Koyfin

And again during the tech bubble burst between 1998 and 2002:

Source: Koyfin

Source: Koyfin

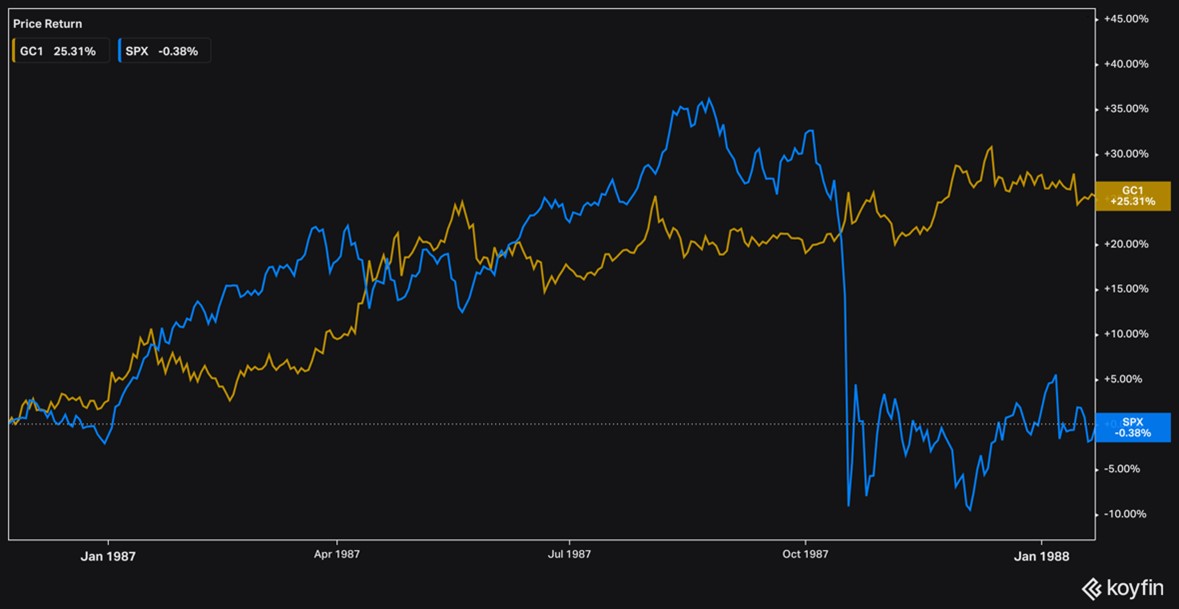

And gold protected you from the sudden plunge of the 1987 crash. In fact, it hardly seemed to notice anything was going on:

Source: Koyfin

Source: Koyfin

Even during Covid when it initially fell with stocks, it rebounded much faster and only fell about 12% at its worst, vs 34% for the S&P:

Source: Koyfin

Source: Koyfin

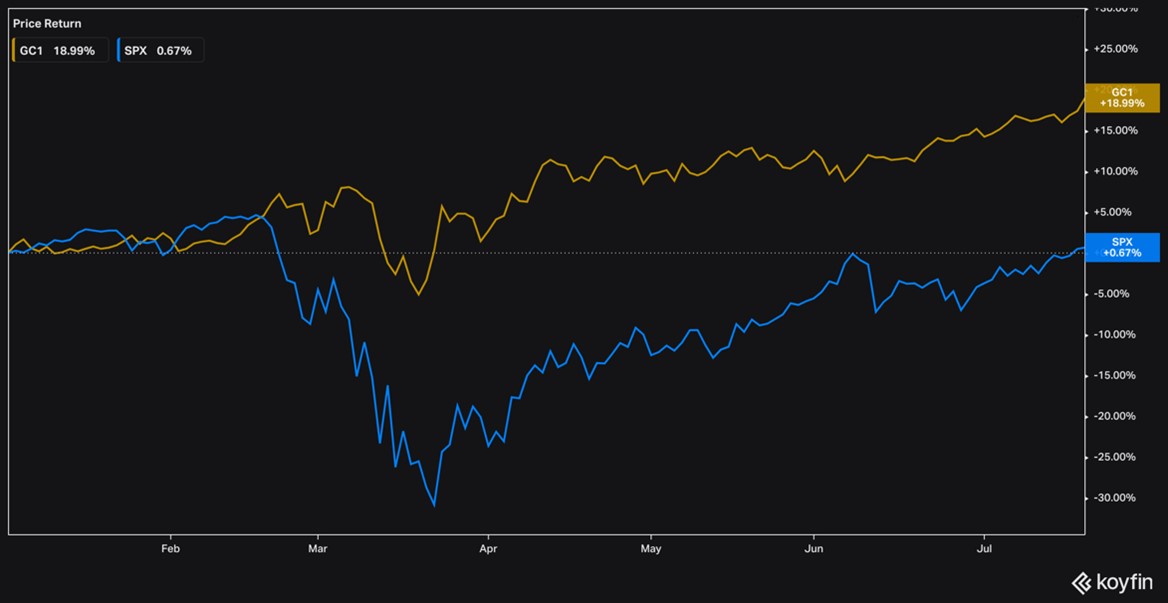

However, this year, they’ve moved in sync to an unusual extent. This correlation is a concern for those who believe gold can hedge against a market crash. But it also calls into question the stock rally – given gold reflects fear of geopolitics and market stress, why are equity markets not responding to those same drivers?

You can see them moving together in 2024 so far:

Source: Koyfin

Source: Koyfin

They also correlated more than normal during the bear market of stocks and gold in 2022, when both declined in surprising unison – although again, gold outperformed:

Source: Koyfin

Source: Koyfin

Is this correlation something to be feared? It’s certainly worth digging into.

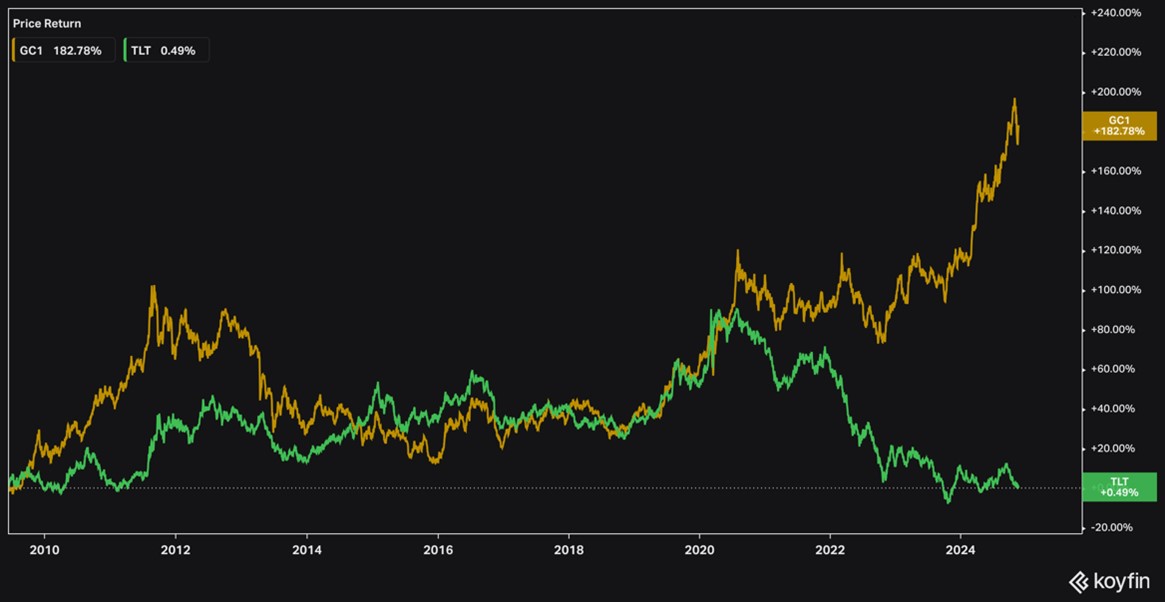

But that’s for another day. Carrying on with today’s theme for now, gold relates to more than just stocks – but also assets like bonds and bitcoin too. Gold and US bonds (green) have diverged lately:

Source: Koyfin

Source: Koyfin

That’s unusual. Gold doesn’t generate any cash flows or return capital to shareholders. They only way to profit is to sell it on to someone else. Thus, when bonds have high yields, and investors can collect 5% annual income easily, that tends to hurt gold.

From late 2020, the price of bonds fell, pushing their yields higher. Gold was surprisingly resilient in this period, as yields went from basically nothing to 5% quite quickly, and gold was flat for two years. Then, once yields stabilised around a year ago, that downward pressure was lifted, and gold soared.

But the level of divergence is now visibly wide. This suggests one or both have gone too far, or the relationship is broken for some reason.

Likewise, when stocks are soaring, investors would usually pull money out of gold and put it into stocks. Seeing them both soar together this year has felt unusual.

Let’s not forget next-generation gold, aka bitcoin. People generally think bitcoin and gold share key drivers (scarcity, inflation) but these two have been taking turns rather than moving together. The best example of this is from the summer of 2020 to 2021. The BOLD ETF, created by our old colleague Charlie Morris at Bytetree, takes advantage of this relationship.

You can see how gold took the lead, before fading back, as bitcoin (in grey) was flat and then took over:

Source: Koyfin

Source: Koyfin

I am also curious about the technical significance of the all-time high phenomenon. Gold nudged up against the all-time high price set in 2020 three more times, before finally breaking higher. It felt like it was building potential energy, which has now released, violently.

I recognise the importance and historical performance of momentum as a factor in all financial markets. However, this felt like a win for the technical analysts who see breakouts about previous long-term highs as significant moments.

Source: Koyfin

Source: Koyfin

Finally, beyond the charts, there is the question of geopolitics. Conflict has taken centre stage once again, in Ukraine and the Middle East. Escalation continues in jumpy intervals, and gold’s role as a safe haven has surely played its part in the recent strength.

So many questions, but who’s got the answers?

There are so many mysteries right now, and the drivers of the gold price seem to have fundamentally changed.

Western institutions are hugely underweight. Central banks are dominating buying. Inflation and interest rates seem to matter far less than they used to. Bitcoin is an emerging competitor. US stock markets are moving up together, but will they go down together? How important are technicals? Is the US stock market as strong as it seems, or is fiat currency just weak?

I am perhaps not the best person in the world to answer these questions, although they fascinate me.

However, we at Southbank Investment Research recently got together an incredible group of experts on gold to answer all these questions and plenty more you might never even think of. They are full of insight and surprise, all hosted admirably by our very own Nickolai Hubble.

To sign up to our exclusive online event, sharing all their interviews, insights and more…

Until next time,

James Allen

Contributing Editor, Fortune & Freedom