Note from John: Before we dive in, I want to make sure you’ve seen the latest advice we’re sharing over at The Fleet Street Letter. Labour’s budget is set to be announced this month – and the simple fact is, they’re after a slice of your wealth. That’s why it’s worth taking the time to take steps to protect your wealth for you and your family, while you still can. Find out how with our eight legal steps to sidestep inheritance tax – all the details on how to access our report are right here.

- Declining energy prices have supported growth

- Yet growth is slowing regardless

- Energy shares are due a recovery

The global economy has been slowing all year despite the mild “tailwind” of declining energy prices. As a key input into all economic output, changes in the price of energy can have a large impact on economic activity and, thus, on the financial markets.

Notwithstanding attempts in many countries to “decarbonise” their economies, oil and gas remain by far the most important sources of energy. As the most widely traded global commodity, oil is the most important energy price benchmark and, thus, arguably the single most important price in the entire world.

This was the topic of an article I wrote last year, titled “The most important price in the world”. Here is a relevant excerpt:

When I was a student of international economics in the early 1990s, my university had a guest lecture programme. Usually once a term, an eminent professor or policy official would visit the school for a day, give a lecture and take part in one or two roundtable discussions.

One guest was Professor Rudiger (Rudi) Dornbusch. Rudi was something of a legend. Not only had he studied under Nobel laureate Robert Mundell “father of the euro” – he had supervised the doctoral studies of several of the most senior central bankers and international economic policy officials in charge of things at the time.

When Rudi spoke, professors and policy officials listened. So did we mere graduate students.

An engaging speaker, I recall precisely how Rudi began his lecture that day. He asked the class a simple question: “Who can tell me: What is the most important price in the world?”

A simple question, but was there a simple answer? The entire class sat in silence.

That silence was broken a few seconds later by Rudi himself, shouting out “Oil! Oil!”

Rudi went on to explain what he meant: oil was the world’s most traded commodity and the world’s largest single contributor to trade deficits and surpluses. Oil price swings had a huge impact on growth, inflation, interest rates and foreign exchange markets.

He then talked us through a whirlwind history of the late 1960s, 1970s and 1980s and showed how every single economic cycle and crisis could be traced back, at least in part, to swings in global oil prices.

It was a tour-de-force modern history of international economics. Before that lecture I didn’t appreciate the central role that oil played.

It still does. Yes, we’re all focused on new technologies and gadgets nowadays, and the possible future transition away from dependence on fossil fuels, but the reality is that oil remains absolutely central to the global economy.

Back when I wrote the above, roughly one year ago, the price of oil was pushing $100/barrel. It fell to under $70 last month. That is a large decline, one that has played a role in the decline in inflation and, by extension, interest rates in the interim.

That, in turn, has helped to support global stock markets. 2024 has been a positive year for shares, with the FTSE 100 total return index up about 10% year-to-date.

Hence, investors should be concerned that, in recent days, the oil price has bounced back sharply. At time of writing, the price is back above $75. This is probably due, to a large extent, to supply concerns relating to the widening conflict in the Middle East.

With the global economy slowing and perhaps even entering a recession, a negative “supply-shock” of this sort could be damaging for stock markets, with one obvious exception: energy.

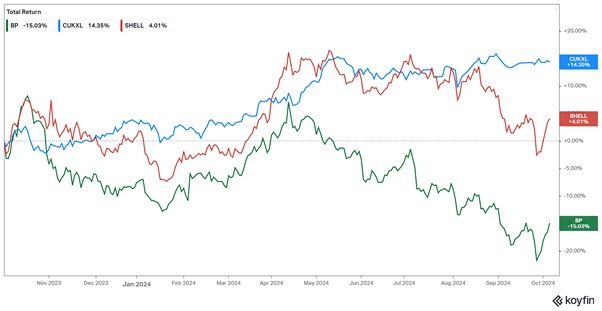

Energy companies have generally trailed the broader stock market over the past year. UK energy giant Shell’s share price is about unchanged. BP’s is down nearly 20%.

Energy underperformance may now be over

Source: Koyfin

Source: Koyfin

If oil prices have now bottomed, as I consider likely, then the energy sector has good outperformance potential from here. It should also exhibit more defensive characteristics than other, more cyclical market sectors such as materials, industrials and consumer discretionary.

In my FTSE 100-oriented investment service, Southbank Wealth Advantage, I’ve recently made the decision to increase one of our Energy company’s target weightings in the portfolio from 10% to 15%. That makes it the single largest holding in the portfolio.

If you’d like to learn more about Southbank Wealth Advantage, you can do so here.

Until next time,

John Butler

Investment Director, Fortune & Freedom