In this issue:

- Southbank held an exclusive, members-only event last week

- Four guest speakers presented on government policy and investing

- Gold, which has been on a tear, was also a topic

This past Tuesday I had the great pleasure to host an exclusive Southbank Investment Research event at a private venue in Covent Garden, the heart of London’s West End. There were nearly 100 guests in the sold-out venue. Many were Southbank Platinum members, who were given RSVP priority.

We had four fantastic speakers share their thoughts and wisdom:

- Steve Baker: former MP for Wycombe, RAF Aerospace and Software Engineer who provides his unique insights over at substack.com/@stevebakerfrsa.

- Alasdair Macleod: Head of Research for Goldmoney, Inc. Prominent commentator on financial, economic and monetary matters at macleodfinance.substack.com. And a member of our very own Global Intelligence Network.

- Jasmine Birtles: financial journalist, author and frequent guest on UK television. Owner of MoneyMagpie.com..

- Dan Denning: financial publisher, entrepreneur, author and contributor to bonnerprivateresearch.com. Dan is also a member of our Global Intelligence Network.

Here’s a photo of all the above, with yours truly in the centre, moderating the discussion:

(If you’d like to learn more about our Global Intelligence Network and unlock how you can access it, click here.)

Yes, there was some doom and gloom about the near-term outlook for the economy, the financial markets and the pound sterling. But there was also much optimism for the longer-term future.

Southbank members had the opportunity to ask questions following the presentations and to have one-on-one chats with the speakers over wine and canapés afterwards. I had several of these myself: chats, canapés and wine.

As a parting gift, all customers also received a complimentary signed copy of my book, The Golden Revolution, Revisited. Steve Baker, who wrote the foreword, also signed some of the books on special request.

Given the positive feedback received, we here at Southbank consider the event to have been a success and we look forward to arranging another one in the not-too-distant future.

Please note that, as with this past week’s event, Platinum members will always be given priority.

Gold goes gaga

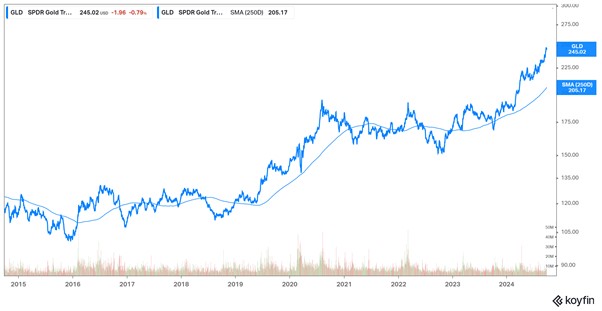

Perhaps not surprisingly, gold figured as a prominent topic at last week’s event. It has been on a tear. Now approaching $2,700 a troy ounce, some argue it is seriously overbought. Others say it is fundamentally overvalued. Is it?

We should first consider which question we are trying to answer. Price and value are not the same thing. Recall Oscar Wilde’s definition of a fool: one who knows the price of everything and the value of nothing.

Is gold overbought? Overvalued?

Source: Koyfin

Source: Koyfin

The chart above certainly makes the case for gold being overbought and thus vulnerable to a possibly imminent correction. A look at 2020-21 is a possible warning in this regard. Gold was comparably above its 250-day moving average prior to a prolonged pullback. The same could happen again.

But consider: there are good reasons why the gold price has been rising. Central banks are cutting interest rates even though price inflation remains positive.

Purchasing power continues to erode. Gold is the classic, tried-and-tested way to hedge against that without simultaneously taking on another risk such as credit default or currency debasement.

There are also geopolitical risks to consider. While there are rumours of possible cease-fires in Lebanon and Ukraine, even if these are true, it is far from clear that any cease-fires at this stage will lead to lasting peace. The world is set to remain a dangerous place indefinitely.

Gold is a hedge against any form of financial instability or monetary mayhem. It’s a rock, after all, one that is uniquely, chemically inert. It is also an alternative international money, one that could be used to avoid economic sanctions, for example.

There is some evidence that, ever since the US became particularly aggressive in applying sanctions when the Ukraine war began, gold has been in demand for use as a dollar alternative. There are also some rumours that, at the upcoming BRICS summit, a gold-backed, multilateral trade arrangement of some sort might be on the agenda.

If so, then gold might just keep on rising as investors prepare for some form of gold remonetisation, at least for international, if not domestic, trade. As the supply of gold is relatively fixed, increased demand for gold as an actual money, rather than a mere hedge, could see the gold price rise by an order of magnitude.

So, returning to the question above, is gold overpriced? Or overvalued? Or neither?

I suppose it comes down to whether one is thinking like a trader or an investor. The former would argue for a consolidation around the moving average to correct what appears, at a glance, to be a seriously overbought condition. The latter would absolutely want to hold a meaningful portion of gold as a hedge against inflation and currency debasement, while also positioning for a possible positive shift in the demand function for gold.

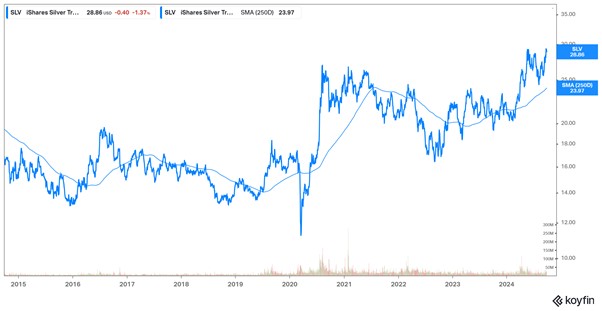

What about silver? Now trading at about $32/troy ounce, it looks historically cheap relative to gold. It also appears slightly less overbought than gold relative to its 250-day moving average. But is silver likely to be remonetised alongside gold?

Is silver overbought? Overvalued?

Source: Koyfin

Source: Koyfin

Probably not. However, silver has a broad and growing number of industrial uses, including in energy, artificial intelligence and medi-tech. And while silver is more plentiful in the earth’s crust than gold, the available above-ground supply is lower.

I, for one, find both metals attractive at current prices, if for the different reasons given above. And what I find even more attractive is the ability to earn interest on both. This is made possible by an innovative, US-based metals firm, Monetary Metals. It arranges for gold and silver to be leased out or borrowed in exchange for interest, which is itself paid in gold or silver.

Monetary Metals is currently offering a three-year silver-backed bond paying an above-market interest rate of 12%. Yes, there are risks involved, which are fully disclosed in the offering. It is, however, a unique opportunity for investors who seek to earn a yield on their metal, rather than merely have it sitting idly in a vault, patiently waiting for it to rise in price. If you’d like to learn more about how to open an account with Monetary Metals and participate in one or more of its offerings, you can do so here.

Until next time,

John Butler

Investment Director, Fortune & Freedom

[Please note, Southbank Investment Research Ltd receives a commission when accounts are made and investments are deposited with Monetary Metals.]