Yesterday’s Fortune & Freedom discussed the case for inflation. Or stagflation – the theoretically impossible combination of rising unemployment and rising inflation.

But what about the evil bugaboo of deflation? That’s what central bankers fear most.

Well, today we begin to make the case for exactly that happening – falling prices and the crisis that entails.

Hold on a minute – you can’t have it both ways. Is it inflation or deflation?

Well, as we made very clear, Fortune & Freedom wants to help you take back control of your money. That means understanding both scenarios. What could make them happen, and what they mean for you.

We won’t tell you exactly what’s about to happen. We don’t know. We can only make educated guesses. As educated as possible is part of our mission.

But you have to decide who’s right and who’s wrong for yourself. Which case is more convincing – in this case the inflation or deflation one?

It’s our job to outline the arguments, tell you what we think (including when we disagree with each other) and then point you in the right direction for what you decide.

That way, even if you disagree, as many readers should and do, you still find value in Fortune & Freedom. Also, if things go as we attempted to predict, or not, you’ll understand what’s going on regardless.

Ironically enough, our view is that you should expect both inflation and deflation. An initial deflationary shock, followed by a government and central bank overreaction which leads to stagflation.

The real question is whether we’ve had the deflationary shock yet. But back to that later in the week.

Who cares about ‘flation?

One thing is clear. The question of inflation versus deflation is both the most boring and important investor question out there. It’s a bit like the wind or the tide. Boring to most of us, but absolutely decisive if you’re a sailor.

So, what would the falling tide of deflation mean for you?

Well, it’s downright dangerous according to some. For a simple reason. Falling prices make debts harder to repay. And so, in a time of too much debt, deflation is dangerous.

Why do falling prices make debts harder to repay? Well, if your employer or you earn less in income each year, then the burden of paying your debt rises. Just as inflation makes debts worth less, deflation makes them worth more.

Of course, there are segments of society which deflation benefits. Like consumers and savers – the value of their money buys more over time. Doesn’t that sound good?

There was deflation during the Industrial Revolution, for example. When goods became cheaper to produce and so prices went down. And Britain boomed. It’s the same story in tech. Consumer prices plunge, although this is masked by the development of new and expensive tech.

So, deflation in and of itself isn’t so bad. Unfortunately, it’s the debt problem that dominates these days. And deflation really would cause a problem given how much debt we’re all in. For governments especially.

By the way, I think we have the deflation and debt problem backwards. Debts are so high because inflation has been presumed. Heck, it’s the central banker’s job to create inflation. That’s why so many people have borrowed so much and saved so little. The Bank of England governor has borrowers’ backs.

If you don’t have to worry about deflation, you can borrow more. The mechanism of lowering interest rates and raising inflation comes at the expense of savers, so people save less.

But, if all that’s the case, why is deflation plausible? If central bankers can create and control enough money to generate inflation, how could deflation emerge?

My answer is that it could strike in a brief shock to the system. But that’s another topic for later in the week. First, you must understand something very simple about our money itself. And how it can disappear.

As sound as the pound?

Since 1931, the pound has had no link to anything of value. This might sound odd. Money is itself valuable, isn’t it?

Well, that’s the topic of a great debate just now. But, for the scope of today, consider this. Money as we know it today used to be convertible to something of value. Gold or silver.

The value of money was determined by how much gold or silver you could convert your banknotes for. The fact that our currency is called the pound sterling is a big hint here.

But never mind big hints. I’ve got something far better. W.R. sent me an email which may be my favourite reader mail ever:

Dear Mr Hubble,

I have been enjoying reading your emails (probably because they echo precisely what I have been saying to people for the last few years).

You may be interested in this; please feel free to use it if you wish, although please keep my address details (on the Bank of England letter) confidential.

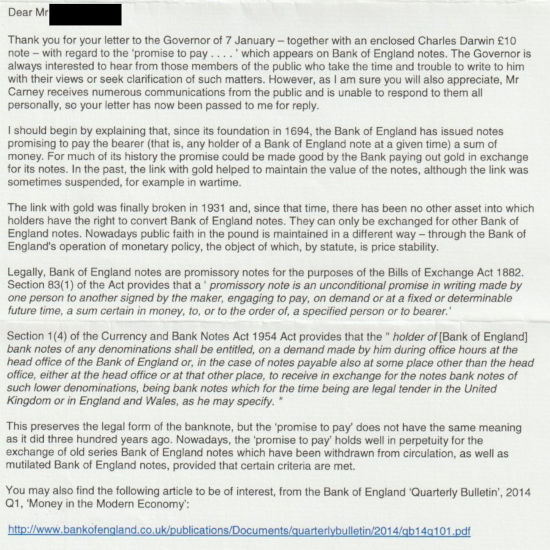

On 7th January 2015 I sent a letter and a £10 note to Mr Mark Carney, then then governor; the text of the letter was this:

Dear Mr Carney,

I enclose a note issued by the Bank of England which bears the inscription “I promise to pay the bearer on demand the sum of ten pounds”, for which I would like to receive money totalling ten pounds. Since the note bears that inscription, I can only conclude, logically, that it is a receipt for money. I look forward therefore to receiving ten pounds of money in specie [meaning gold or silver].

Of course I knew perfectly well that I would only get my £10 note returned, but I was interested to know how exactly they would respond. The reply was interesting, and I think the most revealing parts were these:

The two first sentences of the third paragraph, in which the[y] blatantly admit that the notes have no underlying asset;

The first sentence of the sixth paragraph, in which they say that a promise now is not the same as what a promise used to be;

And of course the last sentence of the third paragraph is highly amusing, since they claim that the BOE’s monetary policy is the maintenance of price stability!

I enclose a scan of the letter for you (page one and two).

With kind regards,

W.R.

Here’s the scan, in which the Bank of England makes all the points I wanted to in today’s editorial for me:

Straight from the horse’s mouth.

The point is that the promise of redeeming your pounds for something of value has been broken, even though it’s still written on all our banknotes. You can only exchange your pounds for more pounds – newer ones in different denominations, but not what the original promise of precious metal entailed. And, importantly, nothing of real value.

Your money now derives its value from the Bank of England’s goal to maintain price stability – no I don’t understand this either. And it is simply incorrect given the Bank of England’s mandate is inflation – the opposite of price stability.

So, if the value of money isn’t backed by an asset any longer, where does it derive its value from? One argument is taxes – you have to pay taxes in government money and that makes it valuable.

These days, money and its value are rather flimsy concepts. Especially because of how it’s created.

The amount of gold or silver used to be a crucial part of deciding how much money there was. This put a natural limit on government money printing. But we don’t have that limit anymore.

So, how is money created now? By the government?

Nope.

Most money is created in the very act of bank lending. And that’s the key to unlocking both inflation and deflation predictions. The amount of lending, and therefore the amount of money in the economy, are not determined by the amount of gold or silver any more. They are now determined by the amount of lending.

The problem with this is that repaying your debts reduces the amount of debt and thereby money in the economy. And that’s how we get our deflationary crash as described in tomorrow’s Fortune & Freedom.

![]()

Nick Hubble

Editor, Fortune & Freedom