In today’s Issue:

- Don’t hold your breath for a gold standard under Trump

- The government needs more inflation to deal with its debt

- Trump’s replacement for Powell will signal gold’s inflection point

It’s like any good murder mystery. Not only is it unclear who dunnit. We can’t even work out why the gold price crashed after Trump’s election.

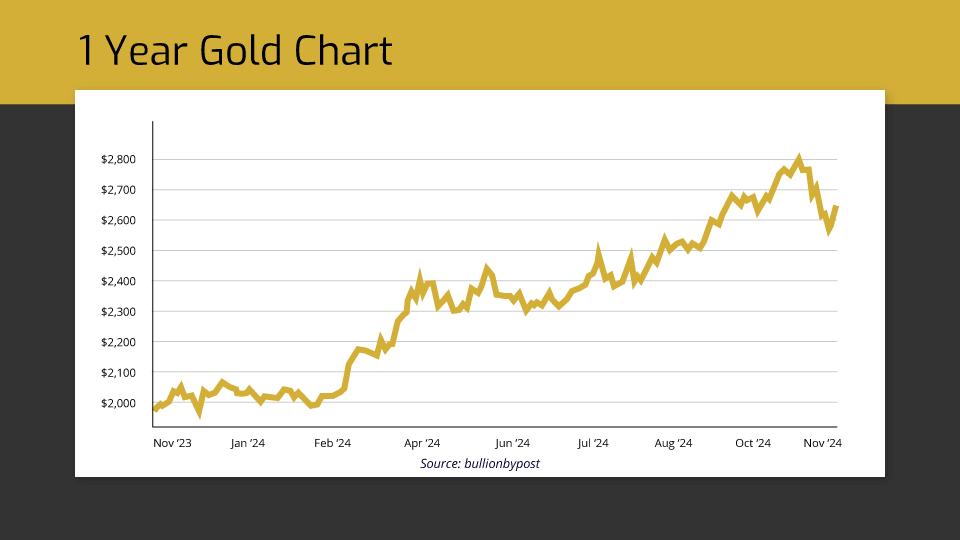

The price fell from an all-time-high of US$2783 to US$2548 in two weeks – about 8%.

Admittedly, gold had been on a tear. Even the world’s most committed gold bugs were getting nervous about a correction.

But why did one come on the back of Trump’s election to President?

There are plenty of theories. Each as unlikely as the next.

A bit of Sherlock Holmes style elimination of the impossible left me with nothing to write about…

An intriguing possibility that I haven’t seen discussed yet is the bust-up between Federal Reserve Chair Jerome Powell and the incoming president.

You see, it’s one thing to tighten monetary policy on a democratic president. Especially before an election. And a woman.

But going after Trump is another matter. Nobody in Washington is going to criticise you for hiking rates on the Don. At least, not openly.

So perhaps gold traders are pricing in the prospect of higher interest rates. Not necessarily on the back of higher inflation, mind you. My point here is that, given the same level of inflation, the Fed is likely more willing to tighten on Trump than they were on Biden and Harris.

Of course, you could argue that inflation really will rise under Trump. His tariffs may raise prices. As could his tax cuts.

But that’s not the sort of once-off price shock which is supposed to move the Fed into hiking rates.

That’s how they got 2021 so wrong. They thought we were experiencing a once-off pandemic and supply chain shock. Not the sustainable sort of inflation they’re supposed to prevent.

When inflation just kept rising, central banks finally took action. Perhaps they’re a little more trigger happy now.

A similar theory argues that the Fed is going to try and engineer a debt crisis on Trump’s watch. A Liz Truss style hit job.

Powell and Trump have already had a public falling out over whether the incoming President can fire the Chair of the Fed. Some say he can. Others that he can’t.

The Fed Chair seems up for a court battle to find out the hard way if Trump makes a move on his job. Trump responded by pointing out a court battle would allow the government to take a closer look at what the Fed is actually up. Something the Fed will be terrified of.

And that brings me to the point I’d like to actually examine a little more closely.

Gold or inflation?

Let’s presume for a moment that the current Fed Chair leaves or is forced out by President Trump in 2025. Never mind how.

What happens next?

There are two possibilities. With very different outcomes. But both of which are good for gold.

The first possibility is the great hope of those who see President Trump as some sort of saviour. He could bring back an advocate of monetary sanity to lead the Fed.

Short odds are for Judy Shelton – a gold standard expert and advocate. She’s also proposed an inflation target of 0%. Which is precisely the opposite to the idea gaining traction elsewhere. Many influential economists want to raise the inflation target.

Obviously, any attempt to bring gold back into the monetary mix would be great news for the gold price. But I think Trump’s fans are kidding themselves.

Gold would undermine the current system. A system which allows the US to finance unsustainable deficits – both trade and fiscal.

Gold would impose a level of fiscal rectitude that even Elon Musk couldn’t deliver given the size of the debt already incurred.

Far more likely is that Trump will pick the opposite candidate. One who will finance his deficits at suspiciously low interest rates.

This would allow his deficit spending to soar, and inflation to make a comeback. Both of which would be his intention.

Inflation is a policy choice

Have you ever wondered why governments and central banks allow inflation to occur? I mean, it’s not exactly rocket science. We know how to stop it.

And yet, the central bankers and politicians who oversaw inflations of the past seemed completely ignorant and incapable. To the point where you have to wonder what was really going on.

The answer is that inflation is one way of getting rid of too much government debt.

There are times in history when debt is so dangerously high that inflation is in fact the less painful means of escaping it.

Of course, during such periods of history, everyone pretends not to understand why the inflation is occurring. They pretend it is temporary. And that someone else is the cause – usually foreigners or speculators.

But this is a charade. And part of the policy.

That’s because inflation only cuts debt if it comes as a surprise to investors. If the government declared its intention to allow double digit inflation for a decade in order to devalue its debt, the whole exercise wouldn’t work. Bonds would crash so far so fast that the rising cost of borrowing would swamp the effect of inflation on the debt.

In some cases, the public catches on and governments are forced to find victims of the inflation scam. That is, they force people to invest in government bonds.

By the time those bonds are repaid by the government, the money is worth a fraction of its former value. And, although investors haven’t lost a cent in nominal terms, their money buys far less.

It comes as no surprise, then, that governments have been legislating left, right and centre to encourage people to invest in government bonds. Banks, insurance companies and pension funds are all on the list of victims once inflation breaks out. Under prudential regulation, they must hold large amounts of bonds. The trap is set. A central banker willing to engineer inflation is all it takes for it to be sprung.

That will be Trump’s plan to deal with America’s debt. All he needs is a central banker to go along with it. To keep interest rates remarkably low, even as inflation rises. To buy the government bonds that Trump needs to refinance. And to pressure institutions and investors into likewise buying them.

It’ll be 2021-2023 all over again. And everyone in government will feign surprise.

The moment Trump appoints his Chair, the market will whiff all this out. Bonds will plunge even further than they already have under Trump. And gold will resume its latest bull market.

No doubt Trump’s followers will be apoplectic. The biggest swing in the vote to Trump came from those who claimed inflation harmed them most. But they’re about to get more of the same.

Like I said, inflation is sometimes the lesser of the evils. Especially if you understand why and use this knowledge so you can protect yourself from the consequences… which is easier said than done.

But here at Southbank, we’re here to help you out.

Starting 9 December, we’re kicking off The Southbank Gold Summit 2025.

In this special 5-day event, the best gold investors and insiders in the world show you:

- Why gold demand could hit an all-time high

- How to profit, even AFTER the price has soared

- The one gold investment to avoid at all costs

And that is just a taste of what you will discover…

Typically, tickets to an event of this caliber would cost £500 each. However, as a valued Fortune & Freedom subscriber, you’re invited to attend for free – but only for a limited time.

Opportunities like this don’t stick around for long. Secure your free seat today before this offer expires!

Until next time,

![]()

Nick Hubble

Editor, Fortune & Freedom