The gold price plunged over 7% in short order from 11 June as the prospect of interest rate hikes in the United States that are sooner than had previously been expected came out of the Federal Reserve’s new projections. Often known simply as “the Fed”, the Federal Reserve is the US central bank.

This is deeply frustrating for gold investors.

Inflation had been surging and interest rates looked to be locked at extremely low levels. It seemed like the perfect situation for gold.

And for a few weeks it was, with the gold price rallying from a double bottom at $1,680 to $1,915 per ounce on 1 June.

Then it all went wrong. But in a strange way.

The explanation for the market action is complex but is intuitive once explained.

So, please read on…

The gold price wasn’t the only thing on the move. Remarkably, long-dated US bond yields fell as the Fed announced it expected to raise interest rates earlier.

This is an odd combination. The threat of higher interest rates in the future because of inflation should not lead to lower long-term bond yields…

Both rate hikes and inflation should raise bond yields.

Thanks to the moves, the gap between inflation and long-term bond yields widened to the largest since 1980.

Investors are buying bonds that pay 1.5% in yield while inflation is at 5%…

Again, this should be the ideal world for gold. But the gold price plunged.

A possible explanation is that financial markets are already pricing in a future crisis triggered by interest rate increases.

It could be that they’ve grown so dependent on excessively low rates, and so accustomed to rising interest rates triggering crises, that the threat of higher interest rates from central banks was enough to cause a panic.

I explained this phenomenon in my book How the Euro Dies:

For 35 years, debt has become steadily cheaper. That’s why the world has seen such an extraordinary debt bloom. Government debt, the average mortgage, student debt, credit cards, corporate debt and every other form of debt have all surged. Especially in Britain.

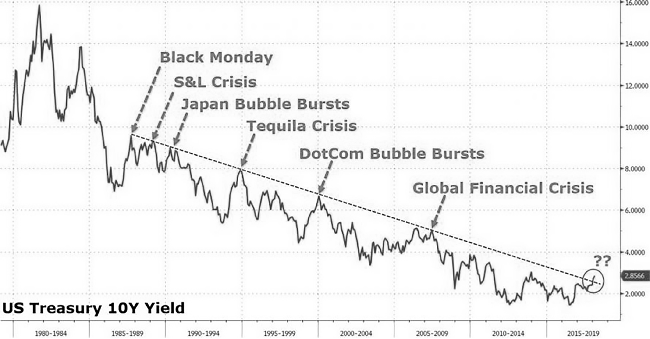

But it hasn’t been smooth sailing. Each time interest rates spiked on their 35-year downtrend, we saw some sort of financial crisis as debtors defaulted. Let’s take a look at the US experience, which dominates interest rates around the world.

Source: Zero Hedge

Source: Zero Hedge

In 1987, the US ten-year Treasury yield spiked from 7% to over 10%. Then came the famous Black Monday, when stock tumbles set records. In the 90s, countries in Asia and elsewhere had their crises each time rates rose. In 2000, the tech bubble burst. In 2008 it was sub-prime borrowers in the US who suffered when rates increased. 2012 it was European governments. We also had the taper tantrum of 2013 when monetary policy was tightened.

Even at today’s ridiculously low interest rates, the phenomenon still plays out. When US and Italian government bond interest rates spiked in early 2018, they triggered a severe correction in stock markets. And led to the “Bloody October”, as an earlier edition of this book predicted. It was the worst period for financial markets since 2008, by many measures. Italy’s economy went into recession, again.

Well, interest rates will eventually enter an upcycle once more. I don’t know whether this will be the beginning of a major bull market in interest rates that will last decades, or just another blip on the 35-year downtrend. I don’t know what’ll cause the spike in rates either. Although we go into some possible contenders below, it doesn’t really matter what the trigger is.

What matters is who blows up first in a world where debt is becoming more expensive. Given the proven propensity of a crisis to occur while borrowing costs are rising, when interest rates begin their upcycle, you have to scour the world for the weakest hands to discover the source of the coming crash.

Is it American sub-prime borrowers, who borrowed more than they can afford based on rising house prices? Perhaps companies, which borrowed too much when times were good? Or tech stock-buying margin borrowers, who face margin calls from their lenders when stocks correct? Perhaps commercial property owners in the new age of working from home and avoiding shopping centres?

In mid-2018 it was Turkey, which had borrowed too many American dollars. As Ambrose Evans-Pritchard wrote at the time, “Turkey is the first big victim of Fed tightening, but it won’t be the last”. Attention immediately turned to Spain, one of Turkey’s biggest lenders, Poland thanks to its external debts, and Italy, because of its precarious banking sector and government financing.

Of course, Covid-19 has worsened the situation dramatically in 2020. It’s adding to debts, shrinking GDP and crushing the incomes needed to pay debts, all at the same time. It’s the perfect storm, but the full effect of Covid-19 is still highly uncertain.

If the consequence of Covid-19’s debts is that markets are so sensitive to higher interest rates that, this time, it’ll take the mere threat of higher rates to trigger the next crisis, then this could explain the recent market action in gold and bonds.

The prospect of higher rates triggering a crisis explains why long-term bond yields fell. Those bonds are considered risk-free, which makes people buy them at the prospect of a crisis.

It also explains why the Federal Reserve is implementing firefighting policies in the repo market to help banks. But that’s another story.

But shouldn’t the threat of a crisis cause the gold price to rise? Doesn’t gold perform well during a crisis?

Well, no, it doesn’t. Gold performs well after a crisis. It is no great crisis hedge in the short term. Instead, the gold price rallies after a crisis because it benefits from the policies which central banks and governments put in place to battle such a crisis. But that’s another story too. Let’s stick with the more recent narrative.

To get a grip of what happens next, ask yourself a simple question: what would 2008 have looked like if central bankers and governments had not allowed Lehman Brothers to fail?

That is what I believe you should be preparing for now.

More on that soon.

![]()

Nick Hubble

Editor, Fortune & Freedom