…and your pension could lose out

When I was first hired by our sister company in Australia, I expected to write about stocks, the economy and financial markets.

Alas, a series of financial crises had other ideas. Politics and central banks drove markets instead, with the occasional crash.

The likes of Greek Prime Minister Alexis Tsipras, Hank Paulson, Ben Bernanke, Matteo Salvini, Mario Draghi and of course Donald mattered a lot more than earnings, dividends and who struck oil.

The threat of bank bail-ins has featured more in my work than bank profits. Trade wars more than Coca-Cola wars. QE more than the price-to-earnings ratios. Sovereign debt more than corporate leverage.

Demographics turned presumed GDP growth rates and “stockmarkets go up in the long run” upside down. And now Covid-19 has overtaken everything else altogether – a pandemic was in nobody’s earnings forecast for FY2020/21.

Over the years, I’ve hesitated about recommending many stocks, despite that being the bread and butter of our newsletter industry. Strangely enough, the FTSE 100 is now trading right where it was when I started writing…

This is of course typical of bear markets. And by bear markets I mean the decades when stockmarkets don’t go up adjusted for inflation, but do a huge amount of booming and busting in the meantime. Rallies that get classified as bull markets and crashes that get classified as bear markets, but between the two, investors on average are going nowhere fast.

That means being an average investor is downright dangerous in times like this.

Is the current bear market for stocks over? When will it be over?

With the US election on the horizon, Donald Trump’s Covid-19 diagnosis, and coronavirus cases climbing globally, you would expect to see markets getting shaky. But so far stock markets are holding steady – at least for now.

Source: Seeking Alpha

But this risks missing the forest for the trees.

Dr Doom and 2008 crisis predictor Nouriel Roubini “Sees a Bad Recovery, Then Inflation, Then a Depression”, according to Bloomberg.

What a time to invest for retirement!

I agree with Roubini. It’s going to get rough out there. The only place to invest in financial markets are the areas that have promise to outgrow everything else around them.

It’s not just Roubini who’s worried. In May, Warren Buffett dumped his airline stocks – $6.5 billion worth. He’s worried the worst isn’t over yet too.

Why? Because there’s still so much we don’t know. And, chances are, something will go wrong.

As the current economic shock continues to unfold, could trigger any number of financial crises, possibly at the same time. Having Covid-19 might not lead to immunity. The economy might not recover anywhere near what stocks are implying. Second waves are playing out already, at least in the UK.

A YouGov poll has found that 53% of Brits are still worried about catching the disease and 65% are avoiding crowded public places – a number that has risen in recent weeks as concerns about a second wave rise. In places that are weakening the lockdown, the awful revival of sales has been as scary as the lockdown.

Not that I blame the lockdown itself for the damage, as bad as a lockdown was. How much of a voluntary self-lockdown would people have imposed in the absence of a government lockdown?

If we’d let the Covid-19 sceptics test the waters for us, while the over-cautious stay at home, we’d have discovered by now who has it right… and the rest of us could’ve adjusted accordingly. Instead, we’re all in the same boat. As though that’s a good thing during a pandemic…

If all that sounds too vague and theoretical, let me ask you this: how many of the last 20 years’ worth of problems have resolved themselves?

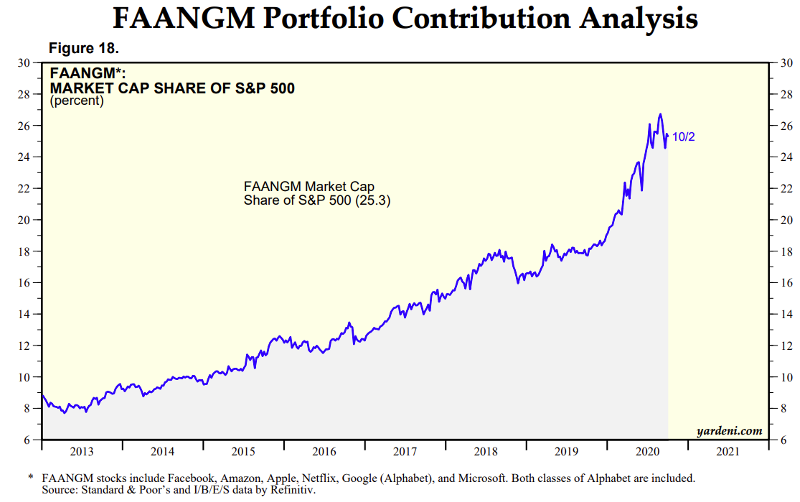

The tech bubble is going strong, with just six companies making up 25% of the US’s S&P 500 index – a higher per cent than in 2000.

Source: Yardeni Research

Year to date, the same six stocks are up 28% while the rest are down 3.6%, which suggests the recovery is iffy.

“Eurozone bailout programme is finally over”, the BBC declared in August 2018. Well, the new Eurozone debt crisis has barely begun. Keep in mind that it’s the second in 20 years and the third if you count the ERM debacle.

According to El Mundo, the Spanish government’s fiscal forecasts imply a bailout, presumably from the European Stability Fund. That in turn requires putting Spain’s fiscal decisions in the hands of the EU. Not great for EU sentiment, nor a coalition government…

Italy is far worse. And don’t even mention Greece.

Tensions are rising within the ECB as some of its more hawkish members – most notably Germany – continue to push for higher rates. Given that deflation continued across the eurozone in September, doves appear to be running out of arguments.

Then there’s the debt and default problem of sub-prime. 2008 was just the warm-up for what’s coming. There could be a bigger wave of defaults for banks and corporate bonds as unemployment spikes.

Pension funds will be ravaged by another failure to deliver the enormous assumed returns they’d used in their funding calculations.

Pensions are funny beasts because of how they function. Few people understand what it means when a pension is underfunded because that’s a surprisingly abstract concept. It involves a lot of assumptions about future contributions, future withdrawals and the return on invested assets. Each of which have a huge impact if you change the assumptions only slightly because all apply to long time periods.

Throw in a tech wreck, a sub-prime crisis, a European sovereign debt crisis or three and a Covid-19 disaster and you get a big problem for those pension balances.

But it’s a problem that plays out in a bizarre way too.

A pension that is disastrously underfunded still has vast assets. It could still continue to pay out for decades. It’s just that, at some point, the fund will be left with no assets to sell and a lot of payouts still to make.

At what point does the pension fund crisis begin?

When the fund runs dry? Unlikely – people won’t contribute to something that’s going down the gurgler.

But at what point is the crisis laid bare? At what point do people realise their pension promises can’t be met? At what point does the lack of future payouts mean the whole thing doesn’t make sense? When will people be furious that pensions paid out vast sums to people who retired years ago, leaving upcoming pensioners with nowhere near enough?

Don’t ask me, I haven’t got a clue when people spot a Ponzi for what it is. They should’ve when it was first announced.

But if you look at company-funded pension plans, that’s where the crisis is likely to begin. When an ever-increasing share of companies’ profits go to topping up pension plans, investors will realise enough is enough.

With all those problems lining up in the financial system and financial markets, it’s no wonder crypto has boomed. A financial system that doesn’t rest on corrupt and fallible institutions, can’t be inflated away and isn’t based on debt is looking like a snazzy alternative.

Best wishes,

![]()

Nick Hubble

Editor, Fortune & Freedom