Today, let’s take time off from the current state of the world… from the recession… from money printing madness… from wondering about family plans and the size of permitted bubbles… from concerns about investing.

Instead, I want to look at something that’s incredibly powerful, that’s all around us, but that most people fail to grasp. If you can get to grips with it then you’ll be well ahead of the crowd.

Maths alert! Yes, some number crunching is unavoidable when it comes to investing. But it’s essential you spend time understanding certain concepts if you want to take control of your money. I’ll do my best to keep it simple…

Let’s start with a thought experiment.

How not to drown at Wembley

Imagine you’re sitting in the very top row of seats at Wembley Stadium, right at the back and far from the level of the pitch. Welcome to the “cheap seats”.

Like other major sport venues, Wembley is huge. It has seating for 90,000 people, you have to walk a kilometre to go around it and you could fit 7 billion pints of milk into the bowl.

Someone will place a single drop of water into the middle of the pitch. One minute later, they will place two drops. A minute after that, it will be four drops. Each minute, the amount of water dropped into the middle of Wembley Stadium will double.

Ask yourself this. If the water couldn’t escape, how long would it be before you have to? Before your seat in the gods was under water?

A few hours? A day? More?

In fact, Wembley would be overflowing with water after just 47 minutes. If you hadn’t brought diving gear, the 46th minute would be your last chance to get out.

What’s more, the situation would change very slowly at first and then change rapidly. After 39 minutes, the stadium would still be more than 99% dry. At 43 minutes, 89% empty. But a mere three minutes later, after 46 in total, it would be 88% full. After 47 minutes it would be fully swamped (as would the surrounds).

This is an extreme example of something known as exponential growth. Over longer periods of time, it affects all sort of things around us.

The British are lucky to live in one of the world’s wealthy countries. But getting there wasn’t fast. It took centuries of industrial revolutions, economic expansion and material progress.

At first – say in the late 1700s – it would have been hard to notice the benefits for most people. But it’s been extremely clear since I was born in 1972. For the most part, people are far better off now than back then (at least, in material terms).

Other examples of exponential growth abound and explain a lot of the issues we hear about. The world’s rocketing population in recent decades… annual global energy consumption… the amount of hot air found on Twitter… the size of the national debt… and so on.

This idea of exponential growth is essential for investors. Although, set in the financial context, it goes by the name of compound growth, or the power of compounding.

You can compound a problem by messing something up even further. With investing, what you’re aiming at is something more positive. You want to compound your profits over time. That means they get bigger and bigger in an average year, in absolute terms.

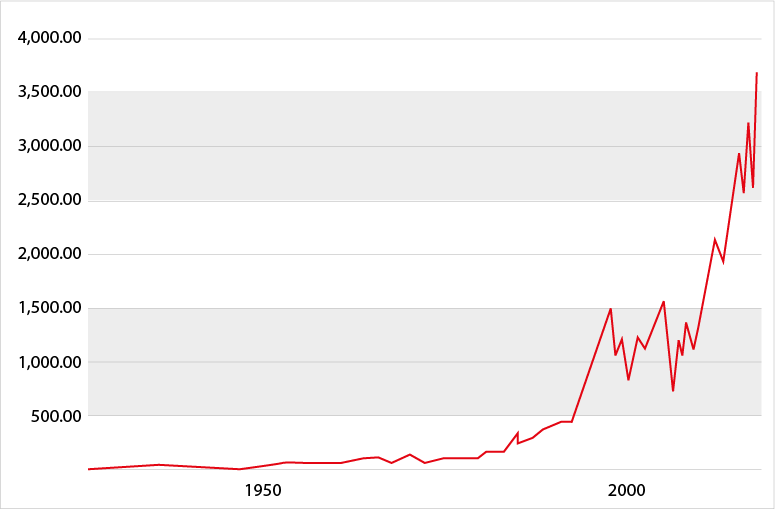

To help visualise what that means, below is a chart of the US stock market from the end of 1927 to December 2020, a span of 93 years.

Compound growth in action

US stock market (S&P 500) –- 1927 to 2020

Data source: Macrotrends

Data source: Macrotrends

Clearly it wasn’t all plain sailing. Sometimes the market got ahead of itself, other times it fell sharply. But the long-term chart has the basic shape that’s characteristic of compound growth over long periods of time. Namely, it looks like a slow build and then a sharp rise, in absolute terms.

This is the power of compounding in action. It’s essential that you think about it when making decisions about what to do with your own money. So let me explain a bit further how it works.

Imagine there’s an investment that will pay you a regular 10% a year. You invest £100 in it. After one year, you make a profit of £10 and now have a total of £110.

You decide to reinvest your profit into the same investment. In the second year, you make a profit of £11 (being 10% of £110), bringing your total to £121. In the third year you do the same, making a profit of £12.10 (10% of £121) taking your total funds up to £133.10. And so on…

Look carefully and you’ll notice something here. Although the rate of growth is constant – the annual profit of 10% – the amount of profit increases each year. First it’s £10, then £11, then £12.10…

The upshot of this is that when investors keep reinvesting their profits then the size of the profits gets bigger over time, on average and all other things being equal.

What’s more, it shows why achieving life-changing results takes time and patience. You need to start investing as early as you can and see it through for as long as possible (until you need the money). But it’s never too late to start.

Of course, in the real world, investments don’t give you the same fixed rate of return each year. Otherwise, the above chart of the US stock market would be a perfectly smooth curve.

Sometimes you’ll make more than average, sometimes less, and sometimes you’ll lose money in a year. But the same basic power of compounding is still in action. If you act consistently, with a solid plan, it will bear fruit over time.

Make mine a double

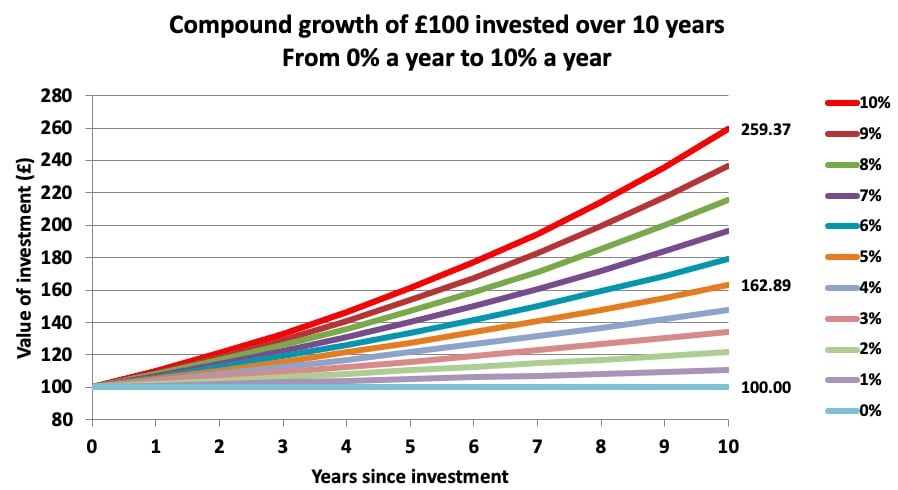

To illustrate the power of compounding further, I’ve put together the chart below. It shows the progression of £100 invested over ten years at rates of return from 0% to 10% a year, with profits reinvested at the same rate.

Source: Fortune & Freedom

Source: Fortune & Freedom

You can see the typical curved outcomes from compounding over time, and the curvature is more pronounced as the rate of return increases.

Note how £100 invested at 5% a year grows into £162.89 after ten years, for a total gain of £62.89 (or +62.89%). Whereas investing at 10% a year grows £100 into £259.37, for a gain of £159.37 (or +159.37%).

The crucial insight is that doubling the rate of return leads to more than a doubling of profits. Over ten years, doubling the annual profit from 5% to 10% increases the total gain by a factor of 2.53 times (159.37 divided by 62.89). The longer that compounding is allowed to work its magic, the bigger this effect becomes.

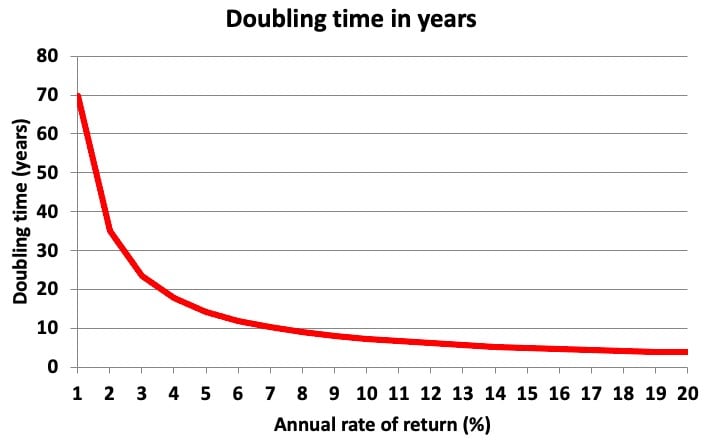

Another way to look at this is to ask how long it takes to double your money at a given rate of return. This is what’s known as an investment’s doubling time, expressed in years. Below is another chart that compares rates of return with doubling times.

Source: Fortune & Freedom

Source: Fortune & Freedom

Unsurprisingly, higher rates of return lead to faster doubling times. But it’s also a very curved relationship on the left-hand side of the chart.

Working out doubling times precisely requires a maths technique called logarithms. But there’s a great rule of thumb that gives a good, approximate answer. I use it all the time. It’s called the “Rule of 70”.

Basically, if you want a decent estimate of how long it will take you to double your money at an expected rate of return, just divide that rate into the number 70.

For example, if the rate is 7% a year, the rule of 70 gives a doubling time of ten years (the precise figure is 10.24 years).

Similarly, if someone promises to double your money in three years, you can flip the formula. Just divide the promised doubling time into 70 to estimate the implied annual rate of return.

Using the rule of 70 gives 23.3% a year (70 divided by 3). Does that sound too good to be true? Probably, in most cases.

(The precise figure to double your money in three years is 26% a year… this method becomes less accurate at higher rates of return. But it’s still a handy guide.)

The most crucial insight is this. Think about the shape of the doubling time chart again.

It tells us that increasing rates of return from very low levels to mid- or high-single-digit levels slashes doubling times.

At 1% a year, using the precise underlying maths, the doubling time is 69.7 years. At 2% it drops to 35 years. At just 5% a year that plummets to 14.2 years. At 10% a year it reduces further to 7.3 years.

In other words, investors in products with low rates of return have an opportunity to dramatically shorten the time to double their money. That’s achieved by finding strategies that lift their average returns from low single digits to high single digits or low double digits.This is a crucial insight in our current, low-yield world.

The obvious mainstream choice is to use the stock market, provided it’s approached in the right way.

It’s a way to put compounding into practice.

If you’re ambitious about your financial future, and you’re looking for regular, deeply researched investment recommendations, I think you’ll like what we have prepared for you.

In fact, I’ve created a wealth building blueprint for 2021, following the principles that have worked for me over the last two decades.

If you’re interested, Nigel has recorded a video message telling you all about it:

Rob Marstrand

Investment Director, Fortune & FreedomPS There are areas of the market I just don’t like the look of right now. Three assets in particular would make me sweat if I owned them. If you have money in the markets, there is a good chance you own at least one of these three “danger zone” investments yourself. When you watch Nigel’s video, you’ll automatically receive a timely report I have created called “Three investments to avoid”.

Watch Nigel’s video now – and the report will hit your inbox within the hour.