Note from the editor: Before we get on to the big news from China’s government, I want to alert you to something our very own government has up its sleeve. My colleague Nick is calling it a “secret tax” and he wants to make sure you’re prepared before it’s too late. He explains all you need to know right here.

In today’s issue:

- China’s three C’s

- Companies, Commodities and Control

- Coming soon, to a country near you?

The big story this past week is China’s big stimulus bazooka, combining both monetary and fiscal support i.e. printing and spending.

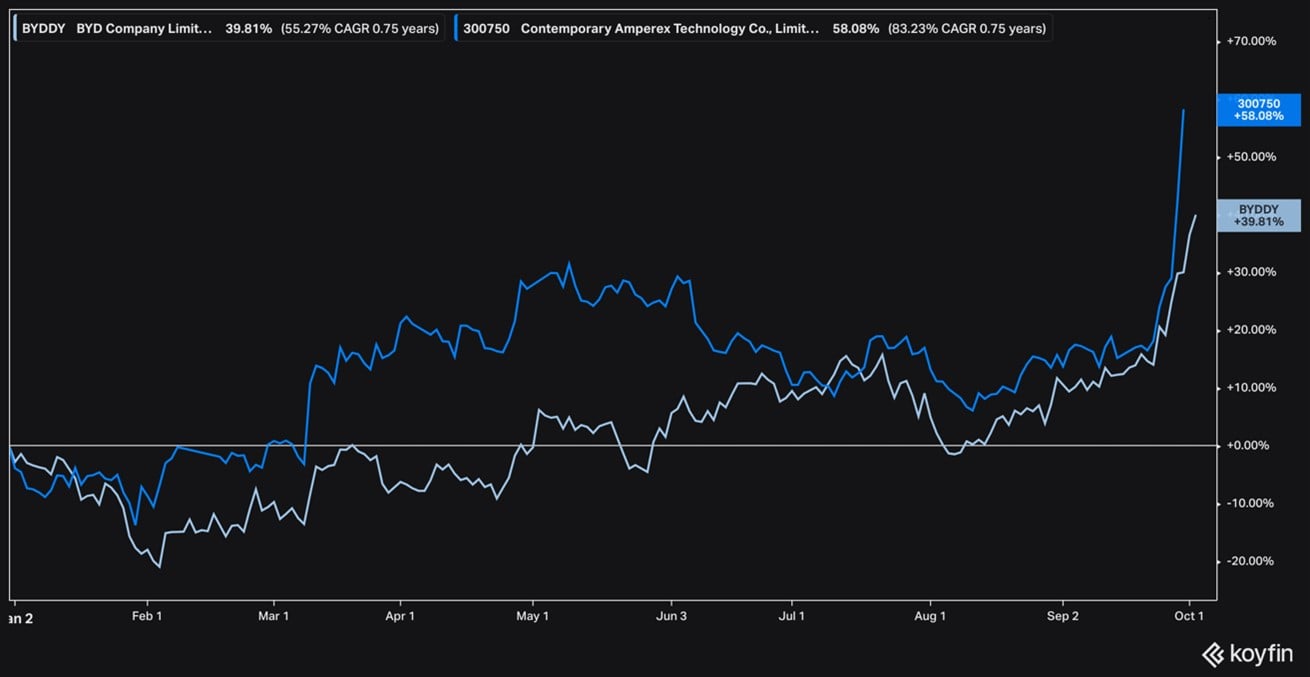

The Chinese stock market rally probably hasn’t escaped your notice but, just in case, take a look at this chart showing the share price performance of CATL and BYD – the top Chinese battery and electric vehicle makers, respectively. They’ve surged 30-40% in days.

Source: Koyfin

Source: Koyfin

But the US also had a big policy boost last month, in the form of a 50bps (0.5%) interest rate cut by the Federal Reserve. Lower interest rates have, in recent history, been key drivers of US stock market outperformance. But this time, Chinese stocks have surged while US stocks hardly reacted.

The difference is valuation. Chinese companies are starting from very low levels, while the US is already “priced for perfection”.

Since the start of the bull market in 2009, this is the performance of China (red) vs the US (blue). A slight gap was opening before Covid, but in the pandemic’s aftermath, a giant chasm has emerged:

Source: Koyfin

Source: Koyfin

In January 2024, Bloomberg reported that the Chinese stock market had never been so far behind the US. At that time, Chinese stocks were valued at 8x earnings while US stocks were 150% more expensive at 20x. Don’t forget that, in the last decade, China has overtaken the US as the world’s largest economy, and has generally shown higher growth.

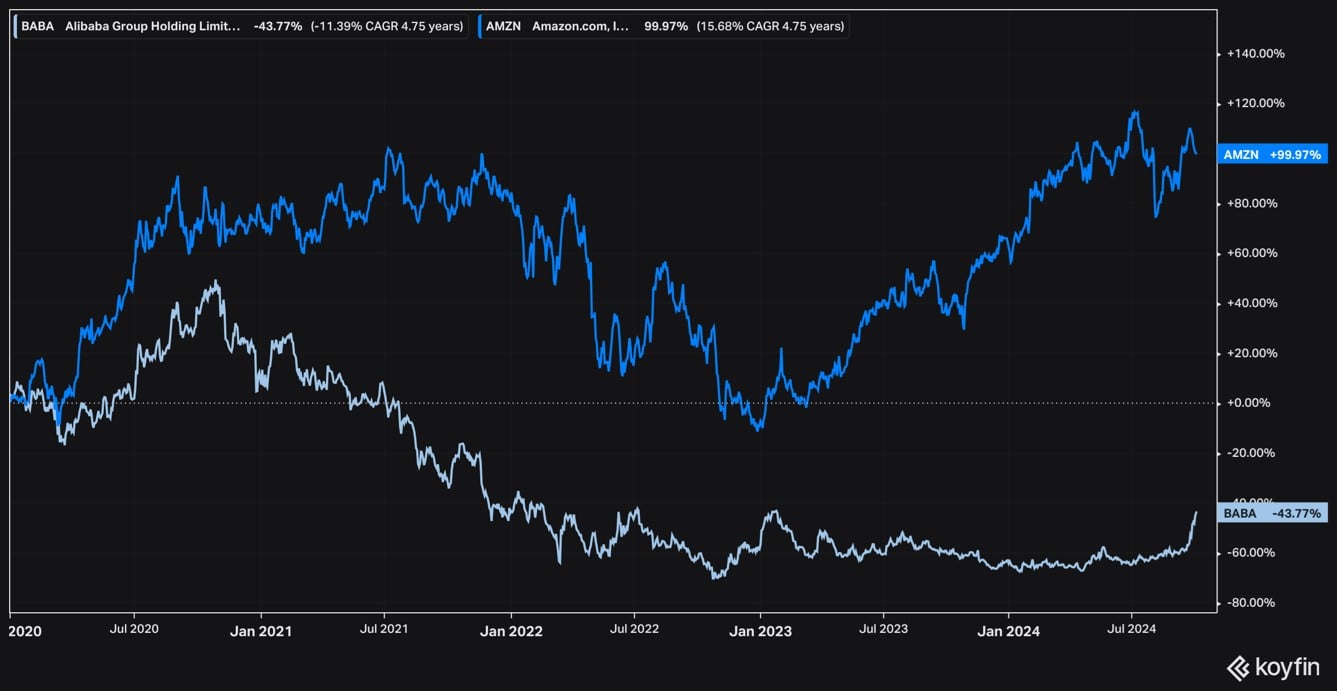

For a more specific example, take Alibaba (pale blue) – perhaps the most comparable Chinese company to Amazon (light blue):

Source: Koyfin

Source: Koyfin

Until the recent stimulus gave it a boost, Alibaba was down 60% since January 2020, while Amazon had doubled. Since 2015, Amazon is up tenfold while Alibaba is flat.

Before the stimulus, there was a point where Amazon’s valuation (using the enterprise value-to-sales (EV/sales) ratio, top panel) was more than three times higher, in relative terms, than Alibaba’s, despite the Chinese firm offering higher cash flow margins (bottom panel, 13.3% vs 8%), as per this chart:

Source: Koyfin

Source: Koyfin

Amazon’s current EV/sales ratio of 3.4x is actually quite low for the US as well. Netflix trades on 8.5x and Microsoft on over 13x. Nvidia’s is 30x…

Using price-to-earnings (PE) ratios, while Amazon was priced at 40x earnings (PE ratio of 40x), you could pick up the “Chinese Amazon” on a multiple of just 8x (now 12x). NFLX and MSFT are both around 33x, while BYD and CATL are around 22x. That’s a 50% discount, even after the recent burst – and despite incredible growth and profit margins in the last decade.

Obviously, there is more to it. Amazon has been doing a better job of growing earnings lately. But the reason Chinese stocks like CATL, BYD and Alibaba have reacted so strongly is because of their low starting valuations. This gives them “potential energy” to rise faster when good news comes around.

China is the dominant player in most energy transition industries such as batteries, electric vehicles (EVs) and renewables. Despite outstripping all global competition, its domestic stocks reflect the wide discount with the US, and plenty of opportunities abound.

And it’s not just companies…

Lithium on the comeback trail

You see, lithium (pale blue) and copper (copper) stocks have surged following the stimulus by their largest customer:

Source: Koyfin

Source: Koyfin

Lithium, in particular, has long been a forgotten trade, having been perhaps the biggest bull market going after Covid. Miners and metal alike went shooting higher as huge shortages were feared in the face of rapidly rising demand. But, as with all such things, direction was mistaken for speed.

Demand has grown quickly (China’s incredible EV adoption has seen to that), but such disparities don’t just take a year to develop. For now, there is enough lithium in the world, and prices had been calming down… until now.

Nickel and rare earth metal stocks have jumped, too. China has many of the dominant companies in the clean energy space, but also represents a huge portion of the demand for and refining of energy transition materials like these.

Across both companies and commodities, the country has built an incredible position of dominance in energy transition industries. The Financial Times recently reported these comments from the CEO of mining giant Rio Tinto:

“While it’s still too early to tell what the outcome of policies like the IRA will be, we haven’t yet seen any significant increase in output. There is currently not enough evidence to suggest western re-industrialisation has taken hold. Western countries can learn from China’s example of replication at scale, delivery at speed and a tightly integrated supply chain with supporting infrastructure”.

China is seen by Western CEOs as an example of how governments can drive economies successfully. But that comes with a price…

The politics of control

As I mentioned earlier, valuation is one reason why Chinese stocks have shown a much larger response to this stimulus than US ones did after the jumbo rate cut. I also mentioned Amazon’s growing earnings were one reason why it had commanded a valuation premium over Alibaba.

The other reason, though, is politics – specifically, the politics of control. The Chinese Communist Party (CCP) plays a large and active role in the Chinese economy.

Alibaba suffered at its hand when its guru tech CEO, Jack Ma, “disappeared” for a few months, amid a hastily cancelled spin-off initial public offering (IPO) of its Ant division, in what would’ve been the world’s largest IPO at the time. (He came back saying rather less-than-capitalist things…)

China suffers because of political risk. It’s hard for companies or investors to get their money out. CEOs and companies remain vulnerable to shifting political preferences. That deserves a discount.

Free markets have driven American companies and share prices ever higher in the last 100 years, while command economies like the USSR and Cuba have collapsed. Warren Buffett says, “Never bet against America” – and this is why.

Until recently, China had been toeing the line between the two quite well, but the bursting property bubble (think Evergrande) led to the current market slump.

Here in the UK, we have a new government that is about to reveal its first budget, and it looks to be shifting more towards the Chinese model than the American one. Much of the concern among investors is about changes to capital gains tax, but changes to inheritance tax (IHT) are perhaps going under the radar.

Labour, along with most developed governments, are in a tricky position. Low growth and high costs mean it doesn’t have enough money. Cutting spending (austerity) was so unpopular that they can’t try that again, which means tax increases are needed.

The inheritance tax changes could, therefore, be significant.

But the good news is that we’ve prepared a clear guide to help you navigate the inheritance tax changes to protect your family’s wealth.

Click here to see how you can get your hands on it.

Until next time,

James Allen

Contributing Editor, Fortune & Freedom