In today’s issue:

- Opposing forces and anti-bubbles

- Buy when there’s oil in the streets

- US exceptionalism: how much longer?

Some people say that the focus on environmental, social and governance factors (ESG) after Covid was a bubble, a marketing mania. If that was true then, what do we call it now that the bubble has burst?

After all, Newton’s Third Law states that for every action in nature there is an equal and opposite reaction.

In financial markets there are bubbles. These are well known, and well discussed.

But as capital is essentially limited, a bubble also sucks money from elsewhere in markets, creating equal and opposite anti-bubbles.

I believe we are now in something of an ESG anti-bubble.

There is plenty of evidence of a backlash against ESG: Unilever, BP, Starbucks and others have all pilled back on their environmental and diversity targets; financial institutions such as BlackRock, Invesco and UBS have cut the number of new funds with ESG mandates; and political attacks in the US have combined with a crackdown on greenwashing in Europe.

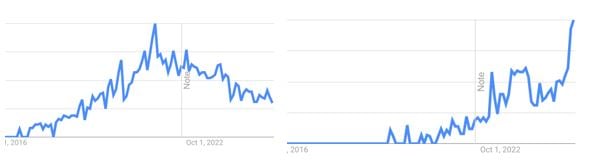

Google Trends captures this nicely using data from Google searches. As per the chart on the left below, it shows how interest in ESG investing has fallen in the last couple of years. Meanwhile in the chart on the right, the phrase “anti-woke” has exploded higher just since the ESG trend peaked. The graphs are on the same timescale.

Source: Google Trends

Source: Google Trends

My suspicion is that just as the ESG phenomenon didn’t last forever, neither will its decline.

It’s just like how bitcoin has been declared both dead and unbeatable more times than you can count.

So how should investors react?

Well, consider George Soros, who famously said that when he sees a bubble, he buys it. That’s because he assumes that he will be one of the first people to see it, meaning the bubble has plenty of room to grow as more people discover it.

Soros is voicing support for momentum investing: the idea that what’s working will keep working.

But an alternative quote which may be just as valid would be, “When I see an anti-bubble, I buy it.”

In fact, one of my favourite investing quotes is from Howard Marks, who said, “When the time comes to buy, you won’t want to,” noting that “all great investments are born in great discomfort.”

This applies in reverse too, thinking about selling near the top: when the time comes to sell you won’t want to.

This line of thinking is backed by the investment theory of mean reversion.

Both viewpoints are valid, in the right context, but timing is important. Just because Soros can buy a bubble when he sees it, doesn’t mean you can.

Mean reversion, meanwhile, has its place. Medium-term cycles drive markets within their multi-decade trends.

Of course, while it looks like the ESG bubble is over, there are plenty of other bubbles and anti-bubbles elsewhere too.

Consider how traditional energy shapes up against clean tech.

Buy when there’s oil in the streets

Back in 2021, a natural resource investor called Goehring & Rozencwajg put out a short note on the anti-bubble in traditional energy. It showed how oil & gas had previously been 16% of the S&P index weight but had then shrunk to just 4%.

No prizes for guessing what happened next:

Source: Koyfin

Source: Koyfin

The energy index XLE is up 200% since then. But for clean energy, it’s been the complete opposite.

Have a look at this incredible chart of what $10,000 would have become in a clean tech index vs the Nasdaq over the last nine years.

Starting in 2016, $10,000 invested in the clean energy index (PBW, orange) would’ve become over $75,000 by 2021, around 2.5x the return of the incredible Nasdaq (blue) which has itself been in an unbelievably strong bull market for 15 years plus.

At that point, it was reasonable to say: bubble.

Source: Koyfin

Source: Koyfin

But by today, that $75,000 has dwindled to just $13,000, an 80% decline over four years, while the Nasdaq has doubled again. Clean tech has gone from a 2.5x outperformance to a 4x under-performance.

I believe that we are in a clean tech anti-bubble.

Creative destruction has occurred, funds closed and naked swimmers have been revealed. Now, the rebirth is coming.

Clean tech firms have come down so much, but almost no one seems to want to buy. Some companies that are really taking off commercially have been ignored and sold for years now. But that might be starting to change.

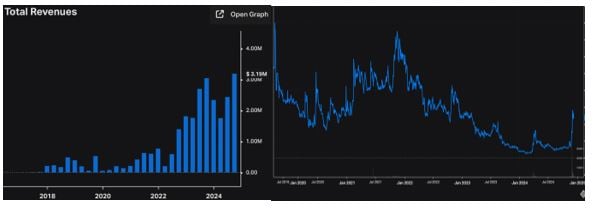

Just look at the following three companies. They have all seen incredible recent sales growth, are forecast to see much more in the near future, and their share prices are suddenly bouncing back from a long, deep depression.

Growth, outlook and momentum, all lining up perfectly.

The first sells batteries for space applications. Its quarterly revenues over the last few years show impressive growth (bars, left) but the share price has only just started to react (line, right). It’s forecast to deliver more, with 70% growth estimated for 2025.

Source: Koyfin

Source: Koyfin

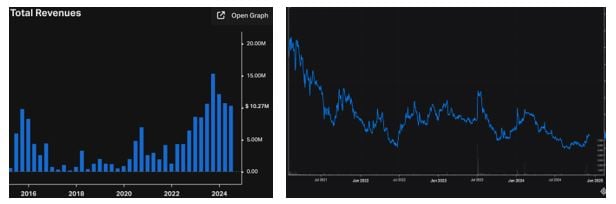

Then there’s this next company, another battery developer. It too has 70% growth forecast for 2025, and has grown impressively already, while the shares have continued to languish. The recent pick-up in momentum is dwarfed by the decline that preceded it.

Source: Koyfin

Source: Koyfin

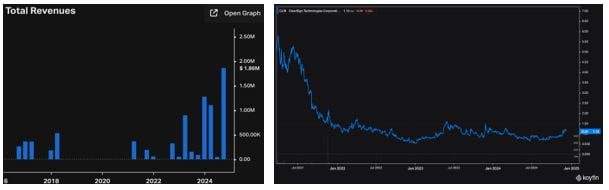

Finally, there’s this maker of emissions-reducing technologies for waste gas emitters. Its revenues have started to jump in the last two years, but there is plenty more to come, with analysts forecasting 10x growth in just the next two years. Once again, the share price is down well over 75% in the last few years, as the anti-bubble has developed.

Source: Koyfin

Source: Koyfin

I believe the time may have come to buy, but investors don’t want to.

This is creative destruction in action.

The bubble burst and the sector went up in flames, not least because the political winds shifted against subsidy-reliant firms somewhat. Those that have survived are birthed in fire, battle-hardened, commercially and technologically ready after four years of development. Moreover, the climate change imperative is even stronger today than it was five years ago. Many are now no longer dependent on subsidies for growth and profitability.

But before you get too excited, it’s important to remember the old investing adage that “as goes America, so goes the world.”

Here with find evidence of further bubble and anti-bubbles.

US exceptionalism: how much more?

Just consider how emerging markets are faring against the US.

Here is Tavi Costa sharing Brazilian valuation vs the US in the last few decades, and here is the chart of the S&P 500 against the MSCI Emerging Markets Index. Both show remarkably clear long-term cycles.

China and the US are two opposing forces at the moment. The US is dominated by tech, China more by commodities and the real economy. Here are the stock markets of China and the US leading up to the financial crisis:

Source: Koyfin

Source: Koyfin

China returned 200% in just a few years from 2003, while the S&P 500 added only 30%.

But here’s what happened next:

Source: Koyfin

Source: Koyfin

The US has enjoyed an incredible run since 2008, up 450%. Meanwhile, the Hang Seng index has only returned 30% in the last 17 years…

In fact, as shown by John Authers of Bloomberg below, the US is completely dominant against all other markets over the last few decades, but since 2010 especially.

Source: Bloomberg

Source: Bloomberg

The markets clearly offer some long-term cycles between various opposing narratives – Brazil, China, the US, bitcoin and ESG. They wax and wane. Where there is a bubble, there is an anti-bubble.

We’ve seen how the largest stock market in the world is in an extremely over-favoured position. If that “bubble” collapses, it may sweep everything away with it.

Of course, the forces of creative destruction are all around us. All over the economy, driven by AI, failure is giving life to newer and better businesses and technologies.

AI is an incredible opportunity, and my colleague Sam Volkering has put together a report on the three companies he thinks can benefit shareholders the most.

Just like the three I showed you above, they are incredibly exciting prospects.

- One company currently controls the rollout of AI across cars, robots and phones

- The second is solving a problem at the centre of AI… and at the heart of civilisation

- And the market for the third company could explode 73 times higher over the next decade.

To find out what they are and why they’re such exciting opportunities…

Capital at risk.

Until next time,

James Allen

Contributing Editor, Fortune & Freedom