In today’s issue:

- Britain is slipping into recession

- The private sector has been contracting all year

- This leaves the stock market vulnerable

We learned last week that, for the second month in a row, the UK economy contracted, if only slightly. Call that stagnation if you like, but there is an even bigger story out there, one that is not being reported by the mainstream financial media.

In the UK, US and much of Europe, in 2024 there was no economic growth at all outside of government. In the US it appears to have been outright negative, with the economy shedding over one million full-time private sector jobs.

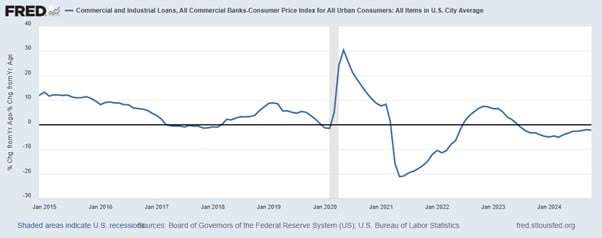

This has coincided with a prolonged period of negative commercial and industrial bank lending growth. Business that are not borrowing are not investing in new facilities and hiring new workers.

Adjusted for inflation, US business loan growth is negative

While inflation has declined this year in the US and the UK, that trend now appears to have come to a halt. The most recent figures available in both countries suggest it might be reversing as we enter 2025. For example, in the US producer prices rose sharply in November. Consumer prices are likely to follow.

In any case, real wages – adjusted for inflation – have been declining and are likely to continue doing so. Adding in the higher tax rates here in the UK, the decline in workers’ purchasing power has been all the greater.

The mainstream financial press has paid only scant attention to all this. Most headlines are about overall growth and jobs, private and public. But while that might give an accurate picture of the economy as it stands today, it provides a misleading image of the future.

The public sector lives off our taxes. It can only grow through increased taxation. Yes, governments tend to run deficits, funded through borrowing. But that is a form of future taxation.

Now, as long as the private sector is growing, then the tax base naturally grows over time, helping to service any accumulated debt and possibly funding more government services. But this is why a private sector recession is so concerning: it outright shrinks the tax base. If the public sector continues to grow, it can only do so by siphoning off scarce economic resources from the private sector.

Once that begins to happen, then higher rates of tax won’t increase revenue. This is one reason why governments frequently look for entirely new things to tax: pensions, inheritance, property, unrealised capital gains… the list goes on and on.

As I predicted some weeks back, given that we are already in a private sector recession, I believe that Labour’s recent tax increases, or any additional tax increases for that matter, will fail to deliver additional revenue.

That’s going to come as a big surprise next autumn. I’m not sure quite how Labour will choose to spin it, but they’ll have to admit that their predictions were wrong, and that borrowing has thus come in somewhat higher than expected.

That may be a problem for the bond market, which in turn might cause problems with the pension funds and insurance companies that were caught out by the severe market reaction to the Truss-Kwarteng 2022 mini-budget.

That funding crisis marked the return of the legendary “bond market vigilantes”. If they pounce on excessive borrowing, pushing up yields, the Bank of England may feel it has no choice but to intervene in the market yet again.

The Bank may already be bracing for this. Earlier this week, the Bank unveiled new lending procedures, signalling that if emergency market support becomes necessary – not just for banks but also for non-bank institutions like pension funds, insurance companies, and hedge funds – they won’t disclose the identities of the recipients.

As Deputy Governor Dave Ramsden explained in a recent speech:

The [Contingent Non-Bank Financial Institution Repo Facility] CNRF will be a contingent facility, available only when activated by the Bank because we judge that gilt market dysfunction is severe enough that it threatens financial stability absent any action by the Bank, and our lending facilities to banks will not, on their own, eliminate that threat.

The design and inherent nature of the CNRF should help avoid stigma: this is a market-wide facility and any use would be indicative of issues in the gilt market as a whole, not problems with any specific firm. To further mitigate the risk of stigma, the Bank intends to publish the number of firms that are signed up to the CNRF, but we would not reveal any names; and in the event that we activate the CNRF, we would only disclose borrowing at an aggregate level.

While the Bank has the power to stabilise the bond market by taking ever more securities onto its own balance sheet, that doesn’t do anything to support healthy, sustainable economic growth. Indeed, one could argue it does exactly the opposite, by denying those sectors of the economy that are productive from being able to access whatever funds they would need in order to grow, or they do so at higher cost.

Economists call this “crowding out”, a situation in which relatively unproductive economic sectors receive favoured access to funds. But this is a recipe for long-term economic stagnation.

The UK has already experienced years of economic near-stagnation. By some measures, the economy has actually shrunk since 2008 once you adjust for population growth. (This growth is something the Office for National Statistics has some difficulty in measuring accurately, as recent, large revisions suggest.)

It may be some time before it becomes clear that Labour’s tax increases have failed to generated additional revenue and that government borrowing is rising above forecast. But this is going to be a big topic this year and one that the mainstream financial media are going to find impossible to ignore.

Corporations are going to struggle to grow profitability in this sort of environment. To the extent that there are inflationary pressures, there is likely to be at least some earnings growth as corporations pass higher input costs through to consumers.

Dividends will still get paid. But valuations, such as price-to-earnings (P/E) ratios for most firms are unlikely to rise.

One exception to this is likely to be the precious metals mining firms. They’ve only just recently starting catching up to the price of gold.

If gold can merely hold its gains from 2024, or rise with inflation, then as we enter 2025 the outlook for the mining firms is excellent. Their P/E lie well below historical averages. Just reverting to the mean would imply a solid performance from here.

Speaking of gold…

At our recent Southbank Gold Summit 2025, experts from around the globe shared bold forecasts, predicting gold’s potential far beyond current levels. But the story doesn’t end there…

Right now, you can access the full summit content, including exclusive member-only interviews, through The Fleet Street Letter.

And here’s the best part: act quickly, and you can still lock in a £150 discount on your subscription.

Don’t miss this chance to gain expert-backed insights and actionable recommendations designed to help you profit from the next phase of gold’s bull run.

Click here to learn everything you need to know.

Until next time,

John Butler

Investment Director, Fortune & Freedom

PS Our in-house crypto expert Sam Volkering is busy preparing an urgent new broadcast. Why so urgent? Because he believes a potentially huge catalyst for bitcoin in January could ignite the next big price eruption. He’s uncovered three ways you could take advantage from the next big move – without buying a single cryptocurrency. It’s clever – and it’s coming soon. Check your email inbox on Friday 20 December for full details.

Capital at risk.