In today’s issue:

- Investors have a habit of chasing returns

- The danger is they overpay for earnings

- That can be avoided by using the golden ratio

For much of the past year the investment mainstream has regularly pointed out that the US stock market is historically expensive.

It is.

Extremely so.

This is largely due to the strong outperformance of a handful of “Big Tech” companies.

Did you know that, following the recent rally, less than 20 US-listed megacaps account for about 75% of total large-cap market capitalisation?

Perhaps this is justified. Perhaps AI and other new technologies will revolutionise entire industries and these megacaps will reap the rewards.

Perhaps, perhaps. There is certainly plenty of hype around.

Let’s see what this all means…

What concerns me is that such hype has begun to look even more extreme than the tech-driven market peak of 2000.

Back then, the top 10% of large-cap companies briefly exceeded 70% of total market capitalisation before the market crashed.

But it never reached 75%, as is the case today.

Stock markets are prone to boom and bust. “Animal spirits”, as John Maynard Keynes called them, come and go.

One investor’s bubble is another’s “new paradigm” of ever higher profit margins and share prices.

We all want to participate in the boom but not the bust. Wise investors accept, however, that precise market timing is all but impossible.

So, what to do? Keep chasing share prices as valuations become ever more concentrated and expensive? Or is it time to get out and possibly miss out on further gains?

Those are tough questions without clear answers. But there is a simple rule that many successful quality- and value-oriented investors follow: don’t overpay for earnings growth.

What price for growth?

All investors seek earnings growth. Large, sustainable share price appreciation is always a function of earnings growth. Hence we should always look for it.

But growth at what price? A rapidly growing company’s share price may rise alongside expectations for even stronger growth ahead. But at what point does the share price exceed even those lofty expectations?

How can we be certain we’re not overpaying for earnings growth?

Well, there’s no such thing as certainty in the investing world. But what we can do is apply a valuation metric that takes all of the above into account: the PEG ratio.

It’s so useful that I sometimes call it the golden ratio.

The PEG ratio divides a typical price/earnings (P/E) ratio by the underlying growth rate of earnings, either trailing or future. The higher the PEG ratio, the more you’re paying for a given rate of earnings growth. The lower the number, the less you’re paying.

It’s a simple adjustment to make. It’s also one that occasionally turns night into day, making an expensive company look cheap, or vice-versa.

Let’s look at a few companies close to home, members of the FTSE 100, and compare their P/E to their PEG ratios.

Let’s start with the UK’s biggest bank, HSBC Holdings plc (HSBA), which has performed well over the past year. The share price (top chart) has risen from around £5.50 to over £8. This has dragged the P/E ratio (lower chart) higher too, from around 6 to 8.

Source: Koyfin

Source: Koyfin

Does that make HSBC more expensive? In a sense, it does. But why not pay more for higher earnings growth? Who wouldn’t pay a little more for a faster growing company?

Now, let’s look at the PEG ratio. Has it also risen?

Source: Koyfin

Source: Koyfin

While it has bounced around a bit on earnings reports and expectation changes, today it’s not far from where it was a year ago.

So, while investors are paying more for the company, they’re doing so in line with the higher rate of earnings growth.

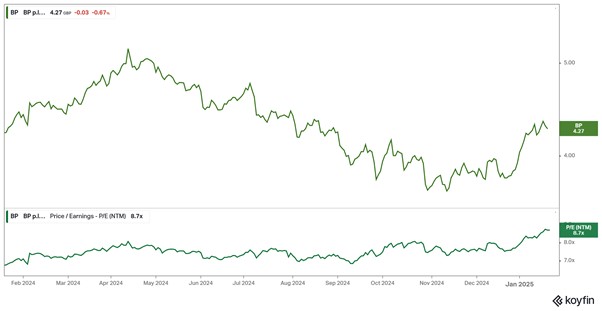

Next, let’s take a look at a stock that, until recently, has struggled: BP plc (BP).

Following a good run in 2022 and 2023, BP slumped for most of 2024 as earnings disappointed. With earnings growth weak, the P/E ratio (lower chart below) steadily rose alongside a declining share price (upper chart below).

Source: Koyfin

Source: Koyfin

So, was BP getting cheaper or more expensive? In P/E terms it was the latter.

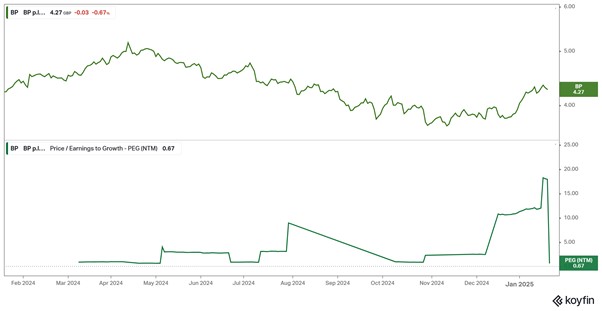

Now, let’s look at the PEG ratio (lower chart below).

Source: Koyfin

Source: Koyfin

As with HSBC, the ratio has jumped around as earnings reports have arrived. Late last year, on disappointing earnings, the PEG jumped higher.

But, following the most recent earnings reports and revisions to earnings growth expectations, it has dropped back to the low end of its range. In fact, it now has one of the lowest PEGs in the entire FTSE 100.

That may be the best explanation for why the share price has recovered sharply of late. Investors see better earnings growth ahead. Hence they’re willing to pay a higher P/E for the company.

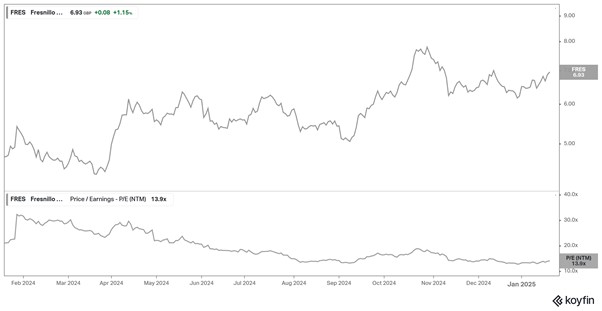

Finally, let’s look at a company I wrote about last week, silver miner Fresnillo (FRES).

Buoyed by a rising silver price, the company’s share price (upper chart below) rose into November before undergoing some profit-taking.

But that wasn’t due to the P/E (lower chart below) moving higher. In fact, following a high starting point, it declined all year as earnings growth expectations rose.

Source: Koyfin

Source: Koyfin

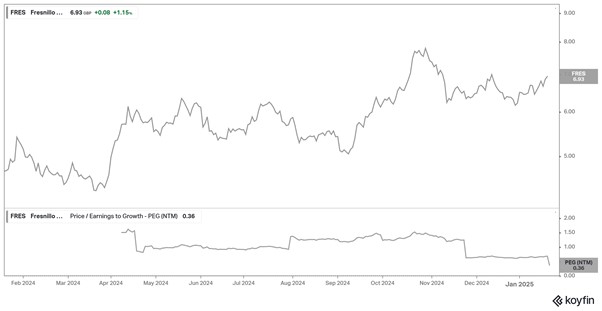

So, is the company now more expensive? Or cheaper? Let’s look at the PEG (lower chart below).

Source: Koyfin

Source: Koyfin

At various times during the year, as earnings reports have arrived and expectations revised, the PEG has shifted lower. It’s now just about the lowest PEG in the FTSE 100, below even that of BP.

What are we to make of that?

The market is probably telling us some combination of two things: 1) it’s not confident the price of silver will continue to rise; and/or 2) Fresnillo’s cost base is going to rise, squeezing profit margins.

In my opinion, I believe precious metals prices including silver will continue to rise this year and probably next. If so, according to the current PEG, Fresnillo is even more of a buy now than it was when the share began to recover early last year.

No financial ratio provides a magical way to know for certain what it going to happen with company earnings growth or share prices. But the PEG ratio provides more information than most.

It’s an essential valuation metric, in particular for relatively mature companies.

However, it has limitations. When it comes to less mature companies, or those undergoing or coming out of a reorganisation of some sort, the PEG ratio is less reliable.

Tomorrow, I’ll discuss another ratio that is more applicable when looking at less mature companies, those distressed or undergoing reorganisation. It, too, isn’t foolproof but is another essential tool for investors.

Until next time,

John Butler

Investment Director, Fortune & Freedom

Bye Bye Biden

Bill Bonner, writing from Baltimore, Maryland

We live in a soap opera country. We live in a social media/cable TV country. In our culture you don’t want to focus on boring policy questions; you want to engage in the kind of endless culture war that gets voters riled up. You don’t want to focus on topics that would require study; you focus on images and easy-to-understand issues that generate instant visceral reactions. You don’t win this game by engaging in serious thought; you win by mere attitudinizing—by striking a pose. Your job is not to advance an argument that might help the country; your job is to go viral.

—David Brooks

Poor Joe Biden. He shuffles off stage… almost completely forgotten, just hours after having been the world’s most powerful man. He has been pulled from the show.

Let’s recall him… before he disappears, like an old shoe swept away at high tide.

Not that there is anything about the man worth remembering. His career was not marked by courage, grace or intelligence. As a member of the Senate for half a century, he was just a willing, even eager, water carrier for the powers-that-be. Almost every dumb proposal, law, budget and program that pains us today has a greasy smudge of his fingers on it.

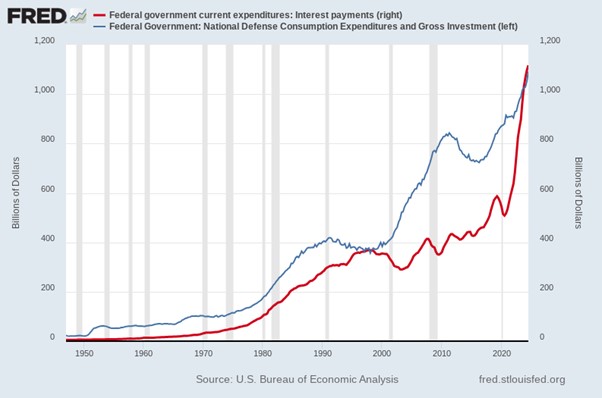

When he was elected, in 1972, the US owed $450 billion. Now, the debt is 80 times higher. Properly invested, that $36 trillion would have gone a long way. It would have built 180 million modest houses, for example. Or, at 5%, it should be paying the US $1.8 trillion in dividends each year. Instead, it was spent on misadventures overseas and stimmy bamboozles at home — most of them approved by Joe Biden. And today, ‘We the People’ don’t get $1.8 trillion in dividends… instead, we pay that much in interest… for which we get nothing.

It’s not pronouns, Panama, or presidential pardons that are most likely to trip up Team Trump. It’s ‘boring policy issues.’ And the legacy of Joe Biden, along with George Bush, Barack Obama and Trump himself. The interest expense on US debt has approximately doubled in the last three years. Soon, it will overwhelm us.

Federal deficit spending over the last eight years has driven interest expense on the debt above defense spending, something that only previously happened at much higher interest rates

And there are only two ways to deal with it. The first and only honest way of bringing it under control is the way Javier Milei is doing it in Argentina. Balanced budgets, he says, are ‘non-negotiable.’ No more deficits. No increase to the national debt. Pay as you go.

The other way is the Biden way… let ‘er rip. Keep on spending. Biden, in his four years, added almost as much debt as Trump ($8.4 trillion for Trump, $7.9 trillion for Biden, roughly).

The first thing we see, looking back at four years of Biden’s presidency, is an almost relentless falsity. Everything he did, said, or failed to say was based on cowardice and mendacity. Even the things said about him were mostly lies. Here’s Kamala Harris:

“Joe Biden’s legacy of accomplishment over the last three years is unmatched in modern history.”

Not so. His accomplishment merely added to those of other 21st century presidents, including the one who both preceded and succeeded him. Otherwise, his policies were predictable… fruitless… and maybe criminal.

When Joe Biden ran against Trump in 2020, his promise was that he offered voters a change of direction. The dumbest thing he did was not keeping that promise.

Coming into office in 2021… he could have easily told the truth. By then, it was obvious. The fight against the Covid virus was a fool’s errand. It didn’t do any good to shut down the economy… the virus didn’t care. Sending out trillions in fake-money on false pretenses — the ‘stimmy’ checks’ — was another colossal error.

Taken together with tax cuts and tariffs, these initiatives added over $7 trillion in national debt… led to the highest inflation in 50 years… and to the slowest GDP growth rates since the Great Depression.

Biden could have distanced himself from the wreck. Instead, like a driver following too close in the fog, he added to the pile up. He stuck with Trump’s tariffs, ramped up spending and amplified the Covid hysteria.

“You’re not going to get COVID if you have these vaccinations,” and “If you’re vaccinated, you’re not going to be hospitalized, you’re not going to be in the ICU unit, and you’re not going to die.”

None of it was true.

Then, Biden offered more money. The American Rescue Act was the third round of stimmy checks, with $5,600 per family of four.

That was almost immediately followed by his $1.2 trillion ‘infrastructure bill’… and his CHIPS act. And then came yet another huge mistake. Forbes:

President Joe Biden signed the Inflation Reduction Act of 2022 into law on Aug. 16.

While its name claims it will tame soaring inflation, estimates show that the bill likely won’t do much to pull down the inflation rate… CBO estimates it will have a “negligible effect on inflation” in 2022, and in 2023 it will change inflation somewhere between 0.1 percentage point lower and 0.1 percentage point higher than it is currently.

Rather than draw attention to the real reasons for the inflation of 2022, Biden signed more jackass spending bills – each one designed to be easy-to-understand, but fundamentally fraudulent and idiotic. Then, as Larry Summers warned, inflation was not Trump’s problem; it was his problem…

And it was bye-bye Team Biden.

Regards,

![]()

Bill Bonner

Contributing Editor, Fortune & Freedom

For more from Bill Bonner, visit www.bonnerprivateresearch.com