In today’s issue:

- IT glitch causes mayhem across European power markets

- French-German power spread hits record peak

- Turning volatility into profits: conditions ripe for batteries

You might not be shocked to read that Europe has never been so disjointed.

And I’m not even talking about politics per se – but about its energy markets, specifically electricity.

At the end of June, an IT glitch on Europe’s biggest power exchange caused the German power price to jump to the highest since August 2022 and several countries to delink.

Day-ahead power on the Epex exchange cleared at €492.04 per megawatt-hour (MWh), while the price in neighbouring France dropped to just €2.96/MWh.

This was the widest spread between the two countries on record.

Day-ahead power markets in central-western Europe have been linked for almost a decade in so-called “market coupling”, whereby an algorithm matches supply and demand across borders.

When it works well, this acts to send electricity to where prices are highest and enables maximum use across the region of low-cost wind or solar energy.

But when it doesn’t, well, mayhem ensues.

On 25 June a technical issue impacted the coupling process, forcing Epex to run separate auctions that ultimately triggered the price discrepancies.

As well as France and Germany, the electricity markets of Austria, Belgium, the Netherlands and Poland were all decoupled, according to Epex.

The decoupling prevented importing, which forced prices up. Electricity auctions then had to be held locally, which meant local surplus and shortage fed into the auction result.

Of course, with different countries employing different generation mixes, local fundamentals dictated widely different prices.

France relies on nuclear plants for most of its power and also has fewer wind farms than Germany, which is also more reliant on coal and gas-fired plants.

In fact, the gap between French and German day-ahead power prices has been widening since March, with the spreads already hitting an 18-year high at the end of May.

“It’s not just about nuclear, it’s the combination of nuclear and hydro output in France… while Germany still needs to import power and start up their coal-fired plants,” Emeric de Vigan, vice president for power and consultancy Kpler, told Montel News.

“France’s merit order is moving away from marginal fossil fuels whereas Germany is unable to do so,” he said, adding that French exports to Germany have been “maximised”, saturating interconnections and leaving no possibility of balancing prices.

The wider backdrop here is that European power supplies are not as robust as they once were due to Germany’s shutdown of its remaining nuclear fleet and the loss of Russian gas exports via the Nord Stream pipes that has squeezed the supply of the fuel available to fire-up Europe’s fleet of gas-fired power plants.

This has left much of Europe increasingly reliant on importing French nuclear power and left Europe as a whole vulnerable to price shocks when supply tightens.

Of course, renewables are also playing a part, especially when wind and solar output falls in Germany.

“Germany are in a position where unlike previous years they will be relying on imports from France for the rest of the year because they have lost a lot of baseload power,” said Icis analyst Robert Jackson-Stroud.

The consultancy forecasts Germany to be a yearly net importer of around 20 TWh at least until 2027, while France is set to export a net 57 TWh each year.

With France’s fleet of nuclear plants now forming the backbone of Europe’s power system, any issues arising from, say, IT glitches at the exchange or French grid constraints has potentially outsized repercussions across the continent.

Indeed, we could continue to see huge price spreads and volatility later this summer when French grid operator RTE plans export curbs due to grid limitations between August through October, a time when countries such as Italy rely on consistent cheap power from France for cooling during hot summer nights and when wind generation tends to drop.

For traders looking to make coin, these are the best of times – or indeed the worst.

In fact, in the aftermath of the fiasco on 25 June, millions of euros were won or lost by traders depending on their respective positions in Germany and France.

“There were winners and losers, depending on what market participants bought or sold… potentially €10-100m depending on the portfolio and hedging percentage,” said a trader based in the Netherlands.

My readers of Strategic Energy Alert recently learnt of a way to play some of this power price volatility in Europe.

Specifically, my recommendation is an owner of battery storage systems that make money by selling power to grid operators or into the market when prices spike.

By owning giant lithium-ion power preserves, operators such as the one I recommended can capture some of the excess intraday demand and benefit from stronger trading power.

My recommendation provides balancing and frequency services that allow it capitalise when shortfalls of power on the network push up both spot prices and so-called “balancing” prices.

In the balancing market, which is used to iron out short-term fluctuations in supply and demand, select companies must be able to respond to grid operators’ demands to increase or decrease power supplies within five minutes’ notice.

If, say, German solar generators less than grid forecasts at the same time as French export capacity falls below normal levels, you can expect these balancing prices to spike.

This means battery operators are effectively paid to be on standby in the event of a sudden drop in frequency, when it is able to provide on-demand electricity in the event of a shortfall elsewhere on the network.

Effectively, the battery allows the operator to capture high returns when power prices intermittently spike – which is exactly what has been happening in recent weeks and months.

Last month prices in Germany’s balancing market hit a peak of €14,978/MWh, just shy of a €15,000/MWh ceiling and potentially a new record imbalance price for Germany. To put this in perspective, these prices were around 200x normal levels.

What is advantageous for my recommendation is that it has relatively little competition. The market for battery storage systems remains underdeveloped in Germany compared to the UK, where the greater prevalence of batteries helps to smooth fluctuations in demand over the course of the day.

But in Germany, there are fewer batteries on the ground that effectively allow operators to buy low and sell high. This can result in spikier prices, much to the benefit of the few that do exist.

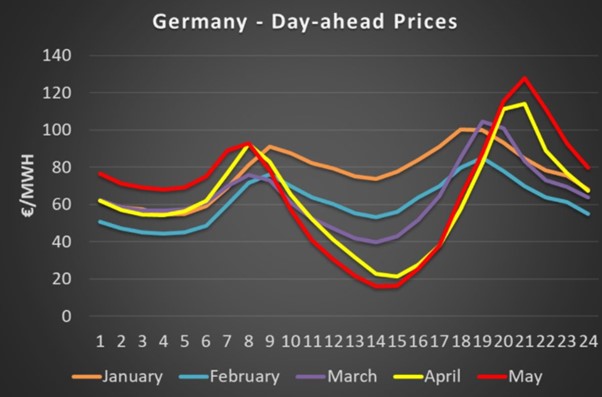

As you can see, Germany is seeing big price volatility this year, with the daily spread in May more than €100/MWh per day on average.

Source: @JomauxJulien on Twitter

After all, for battery owners and operators, volatility is key.

This doesn’t just mean selling power when prices are high, it also means buying when prices are low.

The good news here for battery operators is that the increasing penetration of solar and wind in Germany means that prices can not only move to extremely low levels on occasions when the market is well supplied, but they can even turn negative for short bursts of time, when demand is simply overwhelmed.

Under these circumstances, utilities are actually paying to give away electricity, essentially allowing battery operators to get paid for charging their batteries.

In fact, last year Germany had about 300 hours when prices fell below zero, but this may double in 2024, according to energy analytics firm EnAppSys Ltd.

This is manna from heaven for battery operators on the ground. They can potentially get paid to suck in excess power and then get paid again to discharge when demand peaks above available supplies – win win.

Be clear: battery systems are changing the game of how electricity markets operate.

Already we’re seeing the big influx of battery storage in places such as California dramatically reshape the demand curve and reducing the impact and dominance of fuels such as natural gas, for instance.

In contrast, Germany’s battery energy storage market remains nascent – though the available peaks and troughs on offer in the market mean early entrants can now mop up huge profits.

Until next time,

James Allen

Contributing Editor, Fortune & Freedom