In today’s issue:

- Climate change is changing French wine and the Paris Olympics

- However, bullet and missiles matter more to the energy markets

- Trump, Kamala, and their future foreign adversary

So we’re agreed then. Inflation is over, rates will come down, and everything’s going back to normal.

Or… not?

That is the narrative, so eagerly gobbled up by most market participants. But I can see two things which might derail it. But first, a nod to how climate change is impacting the Olympics.

Soft power

The hot air ballon-cauldron housing the Olympic “flame” is actually renewably powered LED lights and mist, using no fuel or fire for the first time in history. 10,000 free tickets per day have sold out until the end of the games for its beauty and daily twilight ascent.

The games are seeking sustainability on a number of levels: temporary structures, using existing assets (like the Seine for Thursday’s memorable triathlons), renewable energy and recycled materials.

Meanwhile, the torch that lit the cauldron was shaped and coloured like two champagne bottles. Like the Olympics, French wine is another industry that is changing because of climate change.

As temperatures push the optimal geographic band for winemaking further north, Mediterranean nations are losing out and British vineyards are soaring in price, attracting foreign buyers.

We are starting to see real impacts of climate change (on wine) and real solutions to it (at the Olympics) in our everyday lives. As I always say, climate change is far worse than most people think, but the solutions are also progressing much quicker than people realise.

Hard power

The Olympic Games’ push for sustainability in Paris is a form of soft power. Influence through cultural interest and leadership.

But hard power still matters. One of my favourite quotes is from the book Paper Money, by the pseudonymous Adam Smith. He says oil prices were dangerous to predict or trade in the 1970s, because you just never knew whether one morning an oil sheikh would wake up with a bullet in his head.

We are re-living the 1970s in that sense, but countries trade missiles not bullets. Last week, the Golan Heights in Israel were struck by missiles from Lebanon. Israel’s retaliation on Beirut, killing a Hezbollah general based there and possibly a Hamas one too, just ratchets things up another notch.

Once the violence starts, retaliation takes over and people forget why they were fighting in the first place. Momentum isn’t just an investing strategy.

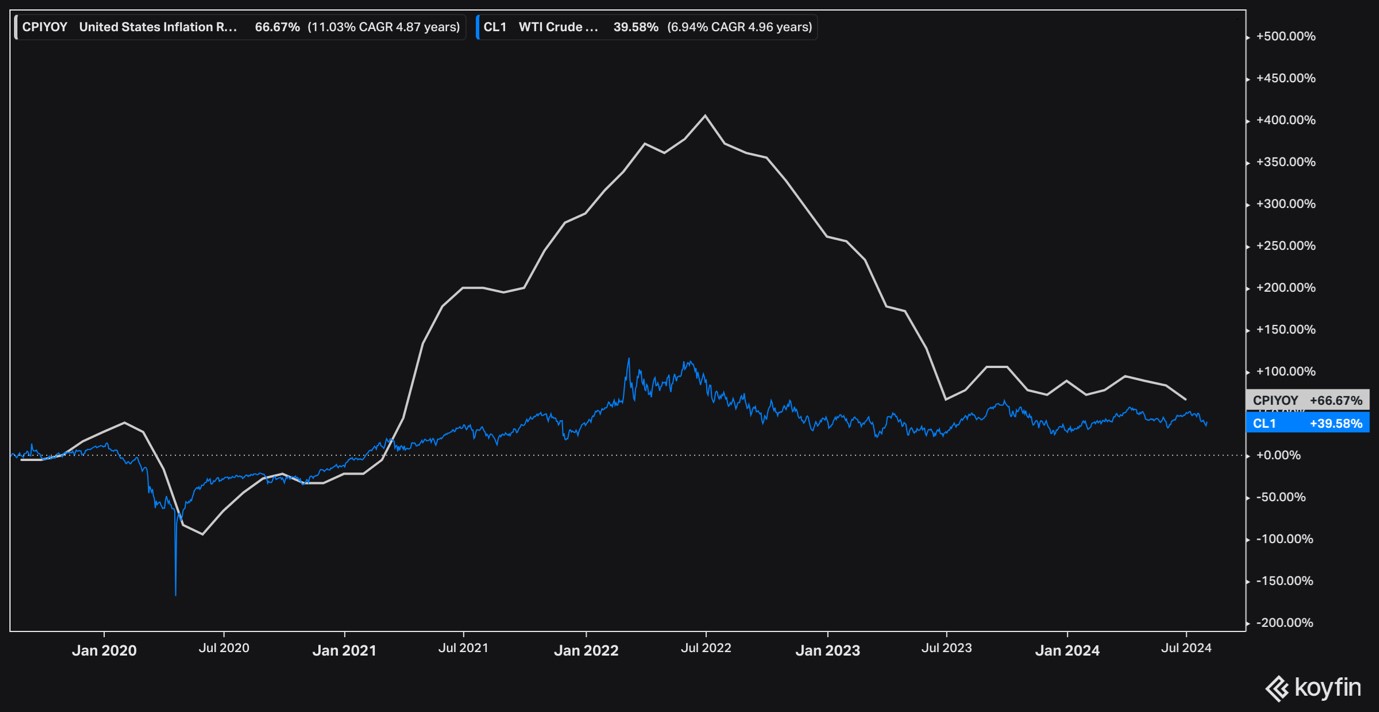

Oil prices abruptly ended their short-term descent on the news. Having fallen lower as earnings season revealed deepening consumer weakness, Brent crude prices reversed higher by 3% last Thursday.

Investors are surprisingly sanguine about Middle Eastern conflict risk at the moment. Oil prices have been in a tight range for almost two years now.

Should we see tensions rise beyond a critical threshold though, I expect that to change. It rose to $120 following Russia’s invasion of Ukraine. If the Middle East sees conflict, the impacts could be far worse, and oil prices far higher.

Inflation

That would also see us return to an inflationary environment.

Oil is the biggest driver of inflation. It is both a component of CPI baskets in the UK and US in its own right, but is also a key cost for most businesses, at least indirectly. When it rises, it’s often passed on to consumers, pushing a broader swathe of CPI basket items up.

Source: Koyfin

Inflation is a risk that investors don’t seem prepared for anymore. It’s over in their heads. “Rates are going low, it’s just a matter of how fast” appears to be the general view.

Consensus this strong tends to be dangerous. I fear that geopolitics are a bigger and more likely risk factor than some people think. If it does come to the worst, oil prices will be an early warning indicator. If it drops out of its current range, perhaps recession risks are rising. But if it climbs sustainably above $80 again, inflation could make a surprise return.

Make America great again, again

The other thing that could surprise that consensus narrative at the moment is politics.

Donald Trump’s near-shooting gave his election odds a boost. Then Kamala Harris’s crowning reversed that move. We’re back to an open race.

Does it matter who wins? Everyone says yes, including the stock markets. Trump is seen as pro-stocks with his tax-cutting pro-business instincts.

He’ll have a mixed energy policy though. He wants to hate the Inflation Reduction Act’s clean energy support, but red states have benefitted greatly from its funding and job creation. He’s all about drilling… But what if financial markets don’t want to fund oil exploration when assets risk being stranded?

Anyway, Nick Hubble thinks politics doesn’t matter anymore. Countries are so indebted, the bond markets decide which policies are permissible or not. Push them too far by cutting taxes and spending too much? And they’ll revolt, sending your interest costs soaring.

The US is running the most remarkable deficits, and in peacetime no less. It’s spending like crazy on the energy transition, international aid, and its own economy. Bond markets have tolerated this so far, because the dollar is the reserve currency, and the US is the most vibrant economy in the world over the last two centuries. Don’t bet against America, says Warren Buffett.

But what about the UK? Bond markets showed Liz Truss who was boss long before the thousands of voters in South West Norfolk did.

Nick says we need to look deeper though. Everyone knows highly indebted countries are slaves to the bond markets.

So, Nick asks, who controls the bond markets?

Whoever that is would be even more important than the prime minister, maybe even the president one day. They’d have incredible power. And we’d want to know what their intentions were, and how they’d affect us.

Nick has gone down that road, and reached some startling conclusions.

You’re going to want to hear this.

Click here to find out more.

Until next time,

James Allen

Contributing Editor, Fortune & Freedom