In today’s issue:

- Intel rode the PC wave but missed the next one

- Investors are rightly excited about the 2023 IPO of a key Intel competitor

- This breakthrough British business is in our portfolio…

Fifty years ago, the greatest invention of the modern world occurred in the tech companies of North America.

Gordon Moore and his eponymous law were key parts of the story of Intel, one of the founding companies of the semiconductor industry.

Half a century on, Intel is increasingly famous for its failures to adapt, loss of competitiveness, strategic blunders and poor investment performance.

So what lessons can be learned from Intel’s rise and fall, and which companies are rising to take its place at the top of the most important industry in the world?

Conducting the global economic orchestra

Semiconductors are perhaps the most important technological innovation of the last quarter century. They are the key to every single piece of technology around us, and without them almost everything we take for granted in modern life wouldn’t be possible.

That makes semiconductors perhaps the most important industry in the world, powering every piece of tech we desire and rely on. But if it’s important, it’s also poorly understood. The industry is so complex and broad that, perhaps until the Nvidia stock craze, many people weren’t very aware of it.

The semiconductor industry started growing through government contracts for military applications, during the Cold War. Only later did companies such as Intel pivot towards consumer products.

In fact, Intel’s story began with the pioneering of the semiconductor industry. Gordon Moore, a co-founder, coined the law of semiconductors that the number of transistors in an integrated circuit would double every couple of years. It was an observation and prediction of a trend, and it has continued far longer than anyone could have imagined.

There are now billions of transistors just a few atoms wide on a single tiny microchip. And this single chip can control your phone signal, camera, music, games, emails, wallet – the lot.

The supply chain includes hundreds of thousands of companies, single machines costing billions of dollars, the most precise light, lasers, mirrors, and chemicals the world has ever known. All driven by Intel’s early innovations and growth.

In the 1980s and 1990s Intel benefitted from being the chip of choice for PC manufacturers. As that market grew into ubiquity, so did Intel, booming to become one of the world’s fastest growing and most profitable companies. But now…

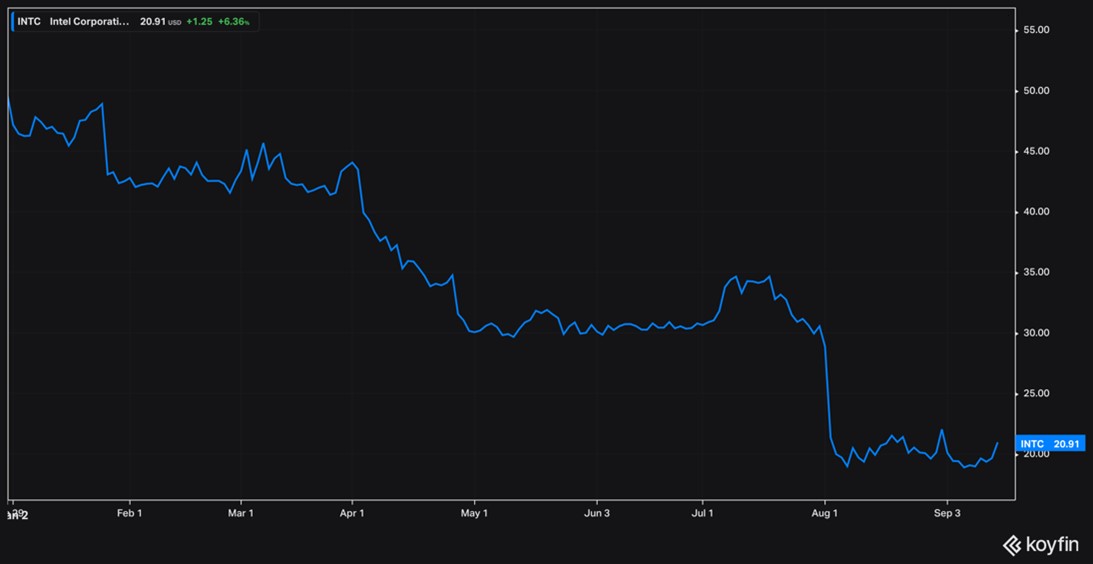

Take a look at Intel’s share price chart for this year so far. It’s down 60%:

Source: Koyfin

Source: Koyfin

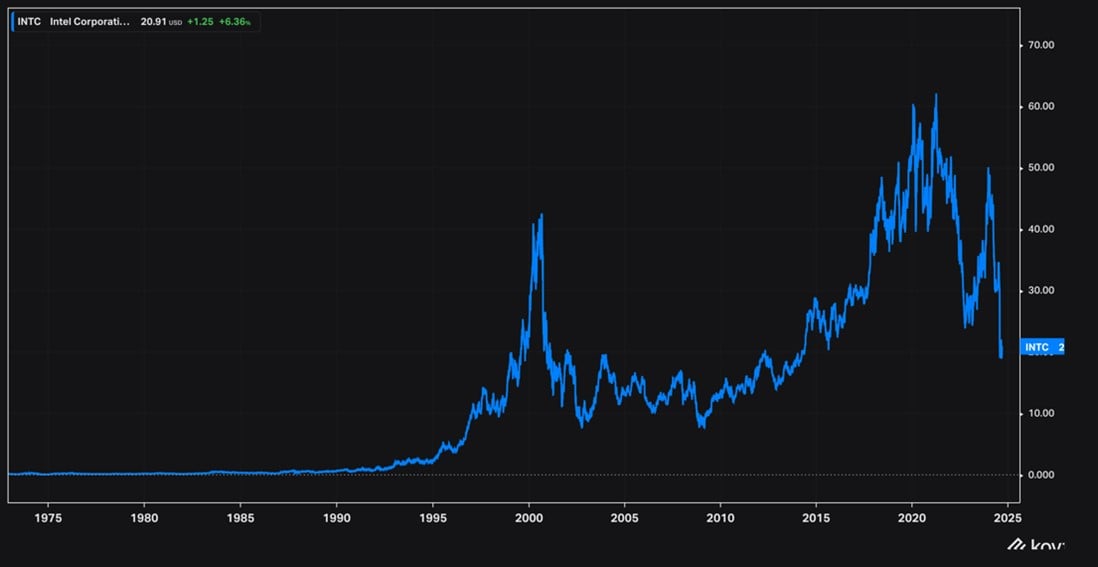

Placed in a longer-term context, the recent fall looks even more abrupt:

It is a classic tale of the life cycle of companies. Extraordinary innovation, brilliant growth, increased complexity, maturity, complacency, errors, changes, reviews and, ultimately, decline and replacement.

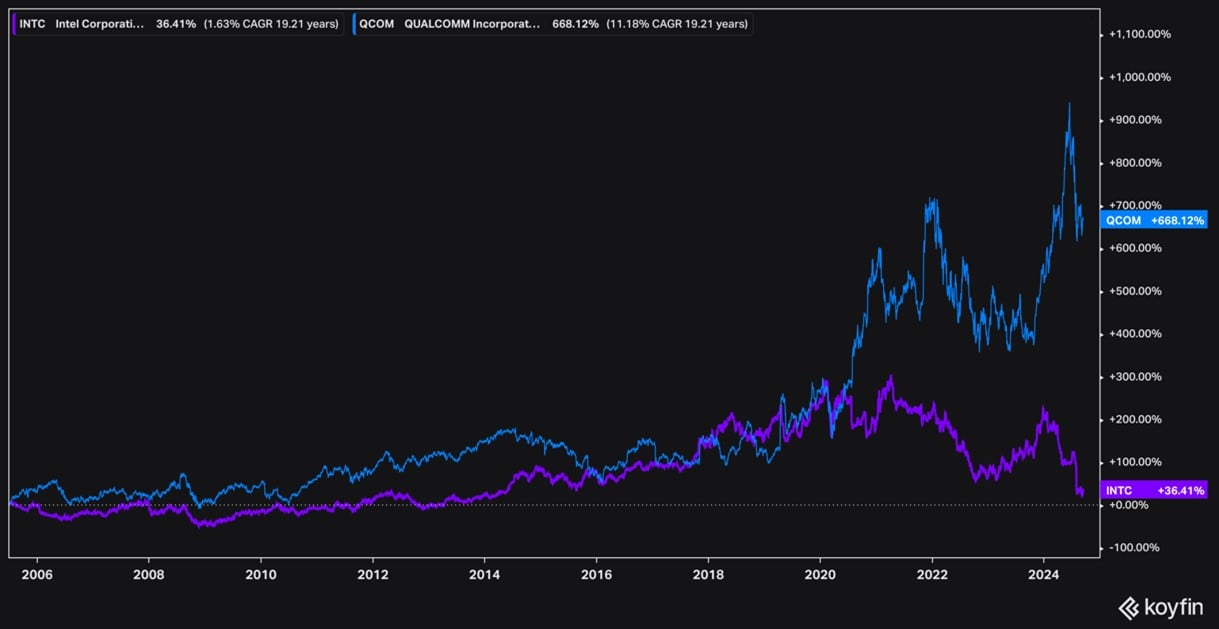

Having surfed the PC wave pre-2000, its problems began when it turned down the chance to be the chip provider to Apple for its new product, the iPhone in the early 2000s. Intel underestimated its potential, so a competitor (Qualcomm) got the contract and never looked back.

Explaining the decision, the then-CEO of Intel, Paul Otellini, put it this way: “The thing you have to remember is that this was before the iPhone was introduced and no one knew what the iPhone would do… There was a chip that they were interested in that they wanted to pay a certain price for and not a nickel more and that price was below our forecasted cost. I couldn’t see it. It wasn’t one of these things you can make up on volume. And in hindsight, the forecasted cost was wrong, and the volume was 100x what anyone thought.”

And that miscalculation has cost investors countless sums. Just look at Intel and Qualcomm’s respective stock performance since 2006:

Source: Koyfin. Qualcomm +688% (blue), Intel +36% (purple)

Source: Koyfin. Qualcomm +688% (blue), Intel +36% (purple)

After 2000, Intel focused on performance rather than efficiency. But as mobile devices took over, efficiency became ever more desirable to manufacturers, leaving Intel behind as new companies rose to take its place.

It followed the playbook outlined in Clayton Christensen’s legendary book, The Innovator’s Dilemma. Quite logically, Intel spent its energy making its products as good as possible for its existing customers, based on their feedback and goals. It was making so much money doing what it was doing that there was no need to look elsewhere.

However, in being so focused on that, they missed the fact that a new and larger customer base was growing to replace the one they served. By the time they realised, it was too late, and the industry moved on to chips for mobile devices without them – to devastating effect.

Indeed, Intel’s time at the top is over. It’s been replaced by upstarts. The semi-conductor industry is now ruled by the likes of TSMC (Taiwan Semiconductor Manufacturing Co), which manufactures chips for other companies, and Nvidia, which both designs and makes them.

A British champion hiding in plain sight

But there is also a British company that is completely central to the most advanced end of the semi industry that is hiding in plain sight.

In fact, it might just be the most important company you’ve never heard of. It doesn’t have a brand, or even a physical product, but its designs are the most sought after in the chip-making industry. Everyone uses them, like Apple, Nvidia, Google, Microsoft, Amazon, Samsung, TSMC and even Intel itself.

This company rose during the very early stages of the mobile era, forming out of Cambridge University. It was completely focused on efficiency and the new mobile customer base, unlike Intel. Today, there are around 7.5 billion chips made every year which use its IP.

By designing rather than manufacturing, it has very light capital requirements, meaning it is incredibly profitable. You couldn’t invest until very recently, as it was privately held. But now you can. At Southbank Investment Research, many of our readers have been able to benefit from its recommendation.

If you’d like to join them, click here…

The evolutionary process of western capitalism continues to fade out the old guard and create new winners. Our investing service is dedicated to finding the latter.

Until next time,

James Allen

Contributing Editor, Fortune & Freedom