In today’s issue:

- Labour’s first budget is pushing the economy into recession

- It has also rattled the financial markets

- This government may be a “one-term wonder”

As 2024 came to an end, I thought its historical significance would be hard to surpass. Yet 2025 has certainly started off with a bang. There has been a fresh fusillade of political fireworks here in the UK. Germany and France are currently in political limbo.

This past weekend, Austria’s “far-right” Freedom Party won the largest share of votes in national elections. The prior week, across the pond, Canadian Prime Minister Justin Trudeau announced that he will step down.

No doubt, more surprises await as the year unfolds. Yet, some events are all too predictable – trends and shifts we’ve seen building for quite some time…

Not a popular term here in the UK, boondoggle is used widely in the US to describe something that is an unnecessary waste of time and money. It can be simply frivolous or something more sinister. But regardless, somebody has to pay.

When applied to political matters, that “somebody” is invariably the taxpayer, whether that is immediately apparent or not. Indeed, modern political art is largely about making popular policy promises that somehow will not cost the taxpayer much, if at all, at least not right away.

In the case of Labour’s first budget, however, the effects seem to be immediate. The British Retail Consortium has attributed poor holiday sales – negative after adjusting for inflation – to Labour’s taxpayer-punishing budget. (One could be forgiven for comparing Rachel Reeves to the Grinch who stole Christmas, something I did recently with Ed Miliband regarding his “green” energy policies.)

To be fair, the squeeze on British taxpayers has been underway for some time. But it is already apparent that Labour have tightened the screws. And it is also becoming clear that, as I predicted immediately following the budget last year, government finances are not going to improve but deteriorate in 2025.

Britain was already teetering on the edge of recession in 2024. Reeves nevertheless raised taxes, something almost certain to push the economy over the edge. As economists generally agree, tax increases in recessions do not raise additional revenue, but they do weaken growth.

As my colleague Nick Hubble and I wrote on multiple occasions last year, recession or no, Britain is already the far side over the “Laffer Curve”, where tax increases no longer increase revenue but in fact reduce it. As the economy slips into recession, this will become all the more evident.

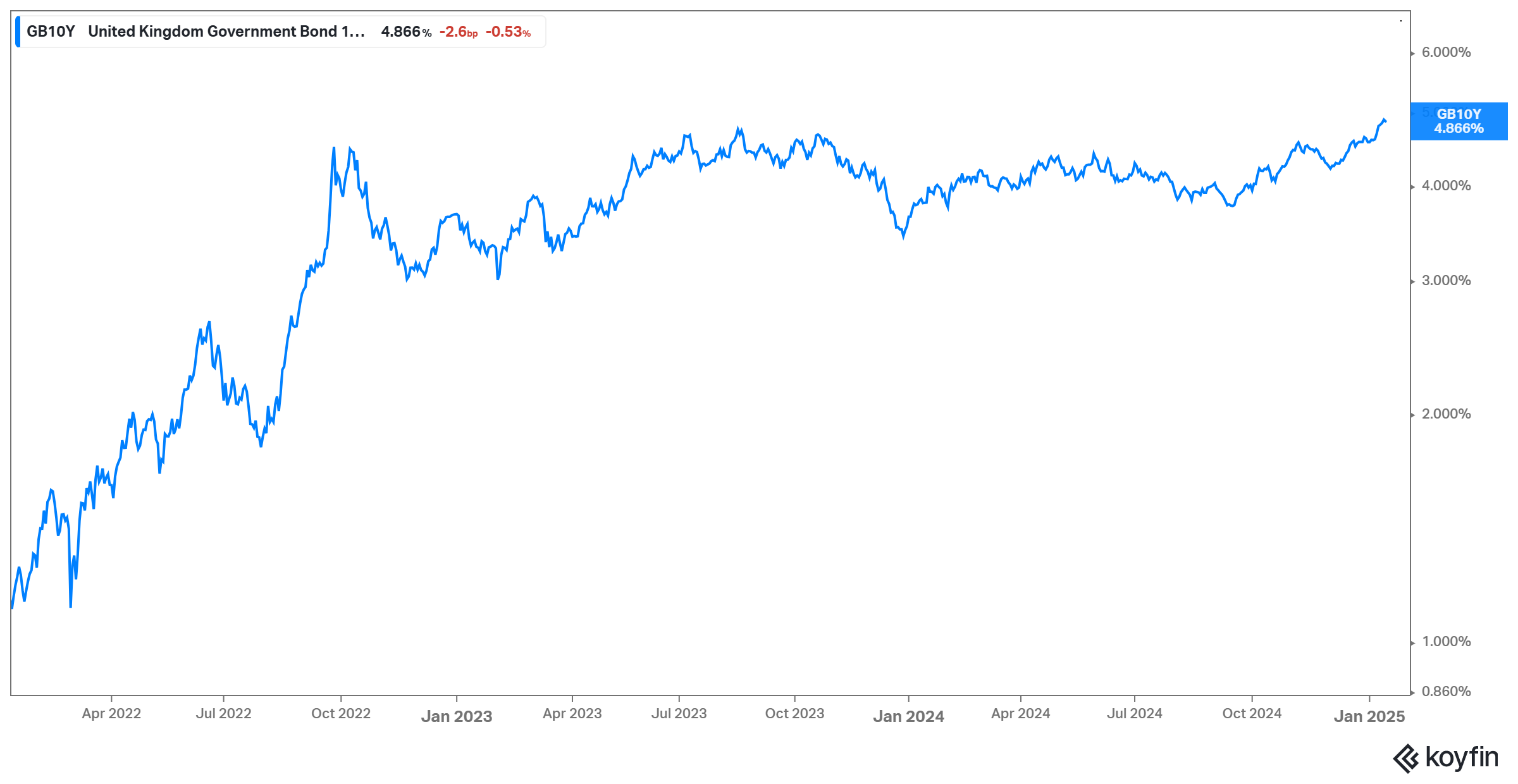

It’s also putting pressure on government finances, a reality the bond market seems to have picked up on. Long-dated gilt yields have been steadily climbing, now surpassing levels last seen during the turmoil that helped unseat former PM Truss in 2022. Meanwhile, the pound continues to weaken.

Some are suggesting this could mark the start of a financial crisis. They may well be right.

10-year gilt yields again on the rise

Source: Koyfin

Source: Koyfin

There are two reasons why bond yields rise: 1) investors expect future growth to be stronger, thereby increasing the demand for capital; 2) investors expect future debt supply and/or inflation to be higher, thus demanding compensation.

These two reasons are not mutually exclusive but, if one were to undertake a simple survey, I think one would find that most believe the recent rise in bond yields is down to rising debt supply and inflation expectations rather than growth optimism.

Regardless, the reality is that the government’s debt servicing costs are now rising, not falling, as anticipated in the budget. They’re already at over 8% of total spending, so we have prima facie evidence that Reeves’ budget is not going to meet with expectations.

Hence rather than closing the “black hole” that she supposedly unknowingly inherited from across the aisle, she’s going to make it even bigger.

Will she then double-down and increase taxes by even more? She might try, but she’ll struggle to get much support from her colleagues, given that Labour are already plunging in the polls. By some measures, this government is already more unpopular than the Labour governments of the 1960s and 1970s. Upstart party Reform is already polling neck-and-neck with them.

Labour seem to be charting a course toward becoming a “one-term wonder” government, potentially cycling through multiple prime ministers, much like the Conservatives before them. It is far from clear what sort of government will replace it, but no doubt the sorry state of the economy and government finances are going to be front-and-centre topics in 2025 and probably beyond.

Until next time,

John Butler

Investment Director, Fortune & Freedom